Auto Insurance News

Introduction

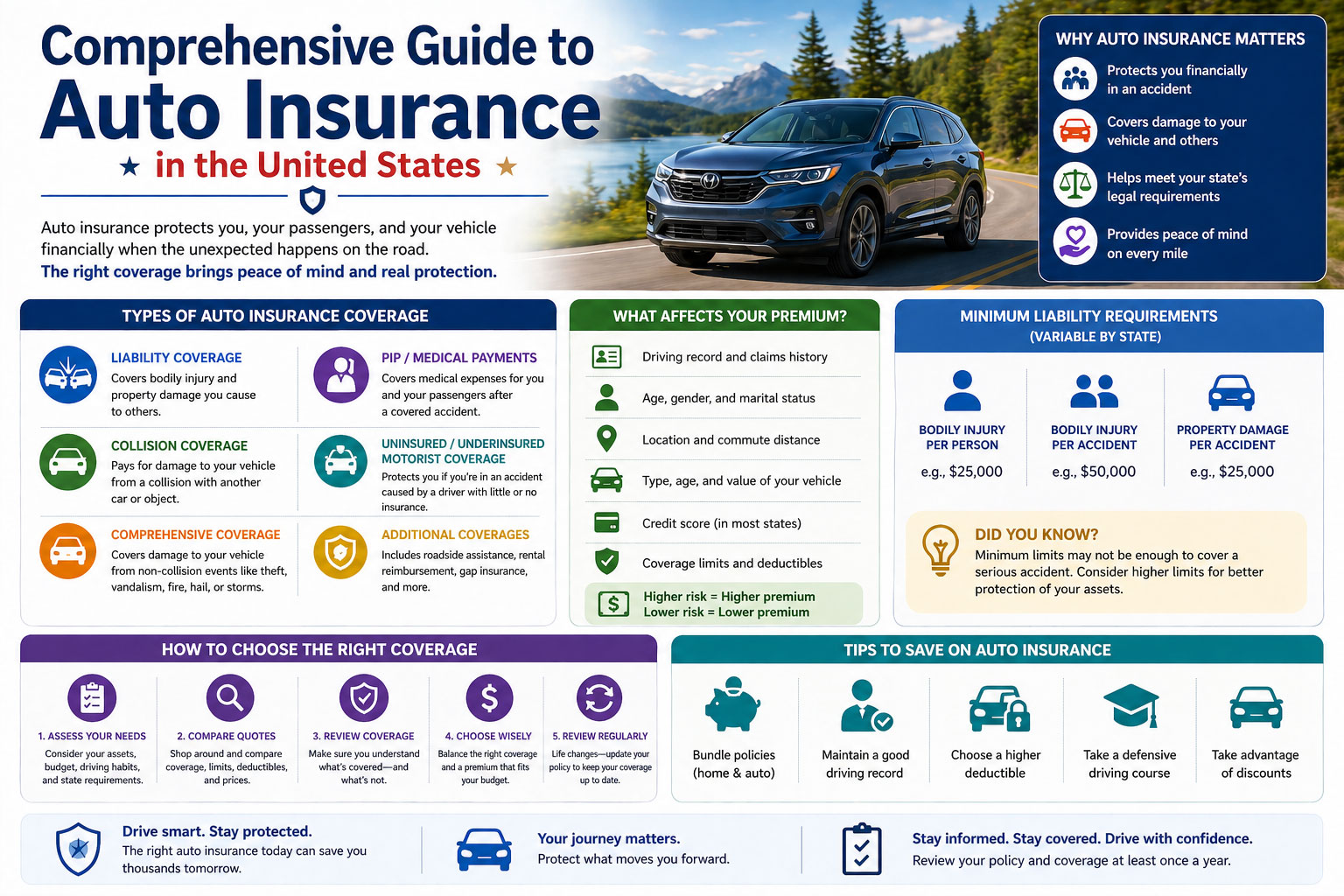

Auto insurance is a financial product that protects you, your vehicle, and other people on the road when accidents happen. Every state in the U.S. requires drivers to carry at least a minimum level of auto insurance, and driving without it can result in fines, license suspension, and serious financial exposure if you cause an accident.

Most drivers need auto insurance as soon as they own or regularly operate a vehicle. Whether you are buying your first car, adding a teen driver to your policy, or switching providers to lower your premium, understanding how auto insurance works puts you in a much stronger position to make good decisions.

Shopping for auto insurance does not have to be complicated. You can compare quotes from multiple insurance companies quickly and easily at autoinsuranceplans.com to find coverage that fits your needs and your budget.

What Auto Insurance Includes

The Core Coverages

Auto insurance is not a single product. It is a bundle of different coverages that protect against different risks. Most policies include some combination of the following.

Liability coverage pays for injuries and property damage you cause to other people in an accident where you are at fault. It is divided into bodily injury liability, which covers medical expenses and lost wages for the other party, and property damage liability, which covers repair or replacement of the other driver’s vehicle or property. Every state requires some amount of liability coverage.

Collision coverage pays to repair or replace your own vehicle after an accident, regardless of who was at fault. If you hit another car, a guardrail, or a tree, collision coverage handles your repair costs after you pay your deductible.

Comprehensive coverage pays for damage to your vehicle from events other than collisions. This includes theft, vandalism, fire, hail, flooding, falling objects, and animal strikes. Like collision, it applies after your deductible.

Uninsured and underinsured motorist coverage protects you when the other driver in an accident either has no insurance or does not have enough insurance to cover your damages. About one in eight U.S. drivers is uninsured, making this coverage particularly valuable.

Medical payments coverage, also called MedPay, pays for medical expenses for you and your passengers after an accident regardless of fault. Personal injury protection, or PIP, is a broader version of this coverage that also covers lost wages and rehabilitation costs. PIP is required in no-fault states.

What Is Usually Extra or Not Included

Several useful coverages are available as add-ons but are not part of a standard policy. Roadside assistance covers towing, flat tire changes, fuel delivery, and lockout service. Rental car reimbursement pays for a rental vehicle while your car is being repaired after a covered claim. Gap insurance covers the difference between what you owe on a car loan or lease and the actual cash value of the vehicle if it is totaled. New car replacement coverage pays for a brand-new vehicle rather than the depreciated value of your totaled car.

Standard auto insurance does not cover personal belongings stolen from your car. It does not cover mechanical breakdowns or routine maintenance. It also does not cover using your vehicle for commercial purposes like rideshare driving unless you have added a rideshare endorsement.

Average Cost Overview

Auto insurance costs vary widely based on your location, driving history, the type of vehicle you drive, and the coverage levels you choose. Here is a realistic look at what U.S. drivers typically pay.

| Coverage Level | Typical Annual Premium |

| State minimum liability only | $400 to $800 |

| Basic full coverage | $900 to $1,400 |

| Mid-range full coverage | $1,400 to $2,200 |

| High coverage with add-ons | $2,200 to $3,500 or more |

The national average for full coverage auto insurance is approximately $1,700 to $2,000 per year, though individual premiums can fall well above or below that range. Drivers with clean records in low-risk states may pay closer to $1,000 annually. Drivers with recent accidents, DUI convictions, or high-value vehicles in urban areas may pay $3,000 or more.

The low end of the range typically applies to older, lower-value vehicles, experienced drivers with clean records, drivers in rural areas with lower accident and theft rates, and policies with higher deductibles that reduce the premium in exchange for more out-of-pocket cost at claim time.

The high end applies to new or high-value vehicles, young or inexperienced drivers, drivers with recent at-fault accidents or violations, those living in densely populated cities with high accident rates, and policies with low deductibles and extensive additional coverages.

Ready to find out where you fall in that range? Use autoinsuranceplans.com to compare quotes from trusted insurance companies and see your actual options side by side.

Key Cost Factors

Several variables have a direct impact on what you pay for auto insurance. Understanding each one helps you make decisions that keep your premium manageable.

Driving record. Your history behind the wheel is one of the strongest predictors of future risk. At-fault accidents, speeding tickets, reckless driving citations, and DUI convictions all increase your premium significantly. A single at-fault accident can raise rates by 30 to 50 percent or more depending on the insurer.

Age and experience. Teen drivers and drivers in their early 20s pay the highest rates of any age group because statistical accident rates are highest in that group. Premiums typically decrease through the 30s and 40s and may rise again after age 70 as reaction times and vision become a factor.

Location. Where you live and where you park your car matters enormously. Urban drivers pay more than rural drivers due to higher accident frequency, higher theft rates, and more expensive medical and repair costs in dense areas. State laws also play a role, since no-fault states like Michigan and Florida tend to have higher average premiums than tort states.

Vehicle type and value. An expensive vehicle costs more to repair or replace, which increases both collision and comprehensive premiums. Sports cars and high-performance vehicles are statistically involved in more accidents and command higher rates. Safety ratings and theft rates for specific models also factor into pricing.

Coverage levels and deductibles. Choosing higher liability limits costs more but provides better protection. Selecting a lower deductible on collision and comprehensive coverage lowers your out-of-pocket cost in a claim but raises your premium. Raising your deductible from $500 to $1,000 can reduce your collision and comprehensive premium by 10 to 20 percent.

Credit score. Most states allow insurers to use credit-based insurance scores as a rating factor. Drivers with lower credit scores typically pay more because insurers have found a statistical correlation between credit history and claim frequency. A few states, including California, Hawaii, and Massachusetts, prohibit the use of credit in auto insurance pricing.

Annual mileage. Drivers who put fewer miles on their vehicles are exposed to less risk on the road and often qualify for low-mileage discounts. Some insurers offer usage-based or pay-per-mile programs that can provide significant savings for drivers who work from home or use their car infrequently.

Coverage gaps. Lapses in coverage history, even short ones, signal elevated risk to insurers. Maintaining continuous coverage, even at minimum levels, protects your rate history.

Ways to Save Money Without Cutting Corners

Know what is required and what is optional. Every state requires liability coverage. Collision and comprehensive are optional unless your lender or leasing company requires them. If your vehicle is older and has low market value, dropping collision and comprehensive and keeping only liability may make financial sense. Use your vehicle’s current value as a guide. If the annual premium for collision and comprehensive exceeds 10 percent of the car’s value, those coverages may not be cost-effective.

Compare multiple quotes before buying or renewing. Insurance pricing varies significantly between companies for the same driver and vehicle. Getting at least three to five quotes gives you a realistic picture of the market and prevents overpaying. Rates also change over time, so comparing quotes at each renewal, not just when you first buy a policy, keeps your premium competitive.

Bundle your policies. Most insurers offer a discount of 5 to 15 percent when you purchase auto and home or renters insurance from the same company. If you insure multiple vehicles, multi-car discounts are also widely available.

Take advantage of available discounts. Common discounts include good driver discounts for clean records, good student discounts for young drivers maintaining a B average or better, defensive driving course discounts, military and federal employee discounts, and discounts for vehicles with anti-theft devices or advanced safety features.

Consider usage-based insurance. Telematics programs offered by many major insurers track your driving habits through a mobile app or plug-in device and reward safe driving with lower premiums. Drivers who rarely speed, brake smoothly, and drive primarily during daylight hours often see meaningful savings.

Raise your deductible thoughtfully. Increasing your deductible reduces your premium, but make sure the savings make sense relative to the increased out-of-pocket cost. Only raise your deductible to an amount you could genuinely afford to pay after a claim.

Common Mistakes and Red Flags

Buying only the state minimum coverage. Minimum liability limits are often too low to cover a serious accident. A minimum policy in many states covers only $25,000 per person for bodily injury, which can be exhausted quickly in a significant injury claim. You would be personally responsible for any costs above your policy limits.

Not understanding what full coverage actually means. Full coverage is not an official insurance term. It typically refers to a policy that includes liability, collision, and comprehensive, but it does not mean everything is covered. Uninsured motorist coverage, MedPay, and PIP are not always included unless you add them specifically.

Letting coverage lapse. Even a short gap in coverage can raise your rates significantly with your next insurer. If you are between vehicles or temporarily unable to pay, contact your insurer to discuss options rather than simply allowing the policy to cancel.

Choosing a provider based only on price. The cheapest policy is not always the best value. A low premium means little if the insurer has poor claims handling, long delays, or a pattern of underpaying claims. Check financial strength ratings and customer reviews before purchasing.

Not reporting an accident promptly. Most policies require prompt notice of accidents and claims. Waiting too long to report can result in a claim denial.

Failing to update your policy after major life changes. Marriage, a new vehicle, a new teen driver, a move to a different state, or a change in how you use your vehicle can all affect your coverage needs and your premium. Failing to update your policy can leave you underinsured.

Frequently Asked Questions

How much auto insurance do I actually need? At a minimum, you need whatever your state requires. Beyond that, a good rule of thumb is to carry liability limits high enough to protect your assets. If you own a home or have savings, consider limits of at least 100/300/100, meaning $100,000 per person, $300,000 per accident for bodily injury, and $100,000 for property damage.

What is a deductible and how does it work? A deductible is the amount you pay out of pocket before your insurance covers the rest of a claim. If you have a $500 deductible and your repair costs $2,000, you pay $500 and your insurer pays $1,500. Deductibles apply to collision and comprehensive claims, not to liability claims.

Will my rates go up after an accident? If you were at fault, yes, in most cases. Rate increases after an at-fault accident typically last three to five years depending on the insurer. Not-at-fault accidents may or may not affect your rate depending on your state and insurer.

What is the difference between no-fault and at-fault states? In no-fault states, each driver’s own insurance covers their medical expenses after an accident regardless of who caused it. In at-fault states, the driver who caused the accident is responsible for the other party’s damages. No-fault states require PIP coverage and generally restrict lawsuits for minor injuries.

How do I find out if a driver who hit me is uninsured? After an accident, exchange insurance information with the other driver. If they cannot provide proof of insurance, contact your own insurer. Uninsured motorist coverage on your own policy protects you in this situation.

Does my credit score really affect my auto insurance rate? In most states, yes. Insurers use a credit-based insurance score that is similar to but not identical to your standard credit score. Improving your credit over time can lead to lower premiums at renewal.

Can I get auto insurance with a bad driving record? Yes, though your options may be more limited and your premium will be higher. Non-standard or high-risk insurers specialize in covering drivers with poor records. Rates typically improve as violations and accidents age off your record.

How often should I compare insurance quotes? At minimum, compare quotes each time your policy renews, which is typically every six or twelve months. Comparing annually is a good habit that prevents overpaying as your driving record improves or your circumstances change.