Collision Coverage

What Is Collision Coverage in Auto Insurance?

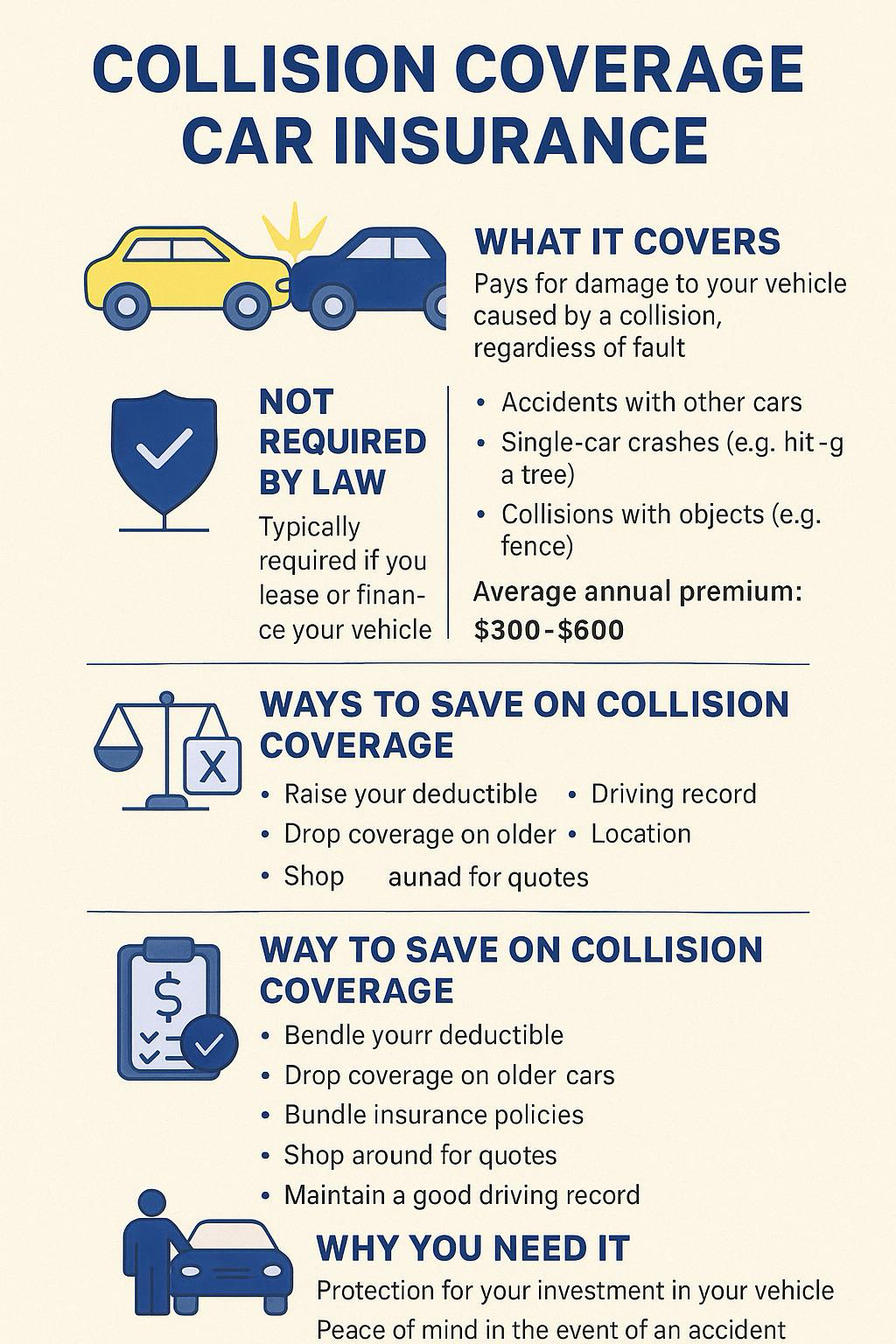

Collision coverage is an optional auto insurance policy that pays to repair or replace your vehicle if it’s damaged in a collision, regardless of who’s at fault. It covers accidents involving:

- A single car crash (e.g., hitting a pole or guardrail)

- Hitting another vehicle (even if you’re at fault)

- Getting hit by another driver who doesn’t have insurance (if you don’t have uninsured motorist property damage coverage)

Important: Collision coverage only applies to your vehicle. It doesn’t cover injuries (yours or others’) or damage to someone else’s car that’s the job of liability and medical payments coverage.

Is Collision Coverage Required by Law?

No, collision coverage is not mandated by state law. However, if you lease or finance your vehicle, your lender will almost always require you to carry it until the loan is paid off. They do this to protect their financial interest in your car.

Once your car is fully paid off, it’s your decision whether to continue paying for collision coverage.

What Does Collision Coverage Not Include?

Collision coverage does not cover:

- Damage from weather (hail, flood, etc.)

- Theft or vandalism

- Mechanical breakdowns or wear-and-tear

- Injuries to you or others

- Damage to another person’s car

For these, you’d need comprehensive coverage, liability insurance, or medical payments/PIP.

How Is Collision Insurance Priced?

Collision coverage cost varies based on several factors:

| Factor | Effect on Premium |

| Car’s value | Higher value = higher premium |

| Deductible amount | Higher deductible = lower premium |

| Your driving record | Accidents = higher premiums |

| Location | Urban/high-traffic areas usually cost more |

| Vehicle type | Sports or luxury cars cost more to repair or replace |

| Age & experience | Younger drivers usually pay more |

On average, collision coverage adds $300–$600/year to your premium, depending on the above factors.

How Much Collision Coverage Do You Need?

You typically purchase collision coverage up to the actual cash value (ACV) of your car. If your car is totaled, the insurer pays up to the ACV minus your deductible.

When deciding whether to carry it, ask:

- Could I afford to replace my car out-of-pocket?

- Is the annual premium plus deductible greater than my car’s current value?

If your car is older and low-value, collision may not be worth the cost. But if it’s newer, financed, or essential to your daily life, it’s usually a smart investment.

Why You Should Consider Collision Coverage

Even though it’s optional, collision coverage can save you thousands in repair or replacement costs. Here’s why many drivers choose it:

- Peace of mind: You’re covered, even if you cause the accident.

- Asset protection: Preserves the value of your car investment.

- Loan/lease requirement: Required by most lenders.

- Comprehensive safety net: Complements liability and comprehensive coverage.

Without collision coverage, you’d pay 100% of repair costs if you back into a pole or get into a single-car accident even if no one else is involved.

How to Save on Collision Coverage

You can reduce your collision insurance costs without sacrificing important protection:

- Raise Your Deductible: Choosing a $1,000 deductible instead of $500 can cut your premium significantly.

- Drop Coverage on Older Cars: If your car is worth less than 10x the annual premium, it might not be worth insuring.

- Bundle Policies: Combine auto and home insurance for multi-policy discounts.

- Shop Around: Get quotes from multiple insurers — rates vary widely.

- Improve Your Driving Record: Avoid claims, tickets, and accidents.

- Choose the Right Car: Cars with lower repair costs and high safety ratings are cheaper to insure.

- Check for Discounts: Ask about safe driver, low-mileage, anti-theft, and loyalty discounts.

Collision vs. Comprehensive: What's the Difference?

| Feature | Collision Coverage | Comprehensive Coverage |

| What it covers | Car accidents (regardless of fault) | Non-collision events (theft, fire, hail, vandalism) |

| Example scenario | You hit a tree | A tree falls on your parked car |

| Required by law | No | No |

| Lender requirement | Often yes | Often yes |

Many drivers purchase both collision and comprehensive for full protection, especially on newer or financed cars.

Final Thoughts

Collision coverage isn’t required by law, but it can be a lifesaver in costly accidents especially when you’re at fault. Whether you're leasing a new SUV or driving a 5-year-old sedan, it’s worth evaluating your needs and budget to decide if the protection is right for you.

For peace of mind and protection of your vehicle investment, collision coverage can be well worth the added cost — especially if you can reduce that cost using the strategies above.