Personal Injury Protection

Personal Injury Protection (PIP) Insurance: What It Covers, Who Needs It, and How to Save

What Is Personal Injury Protection (PIP)?

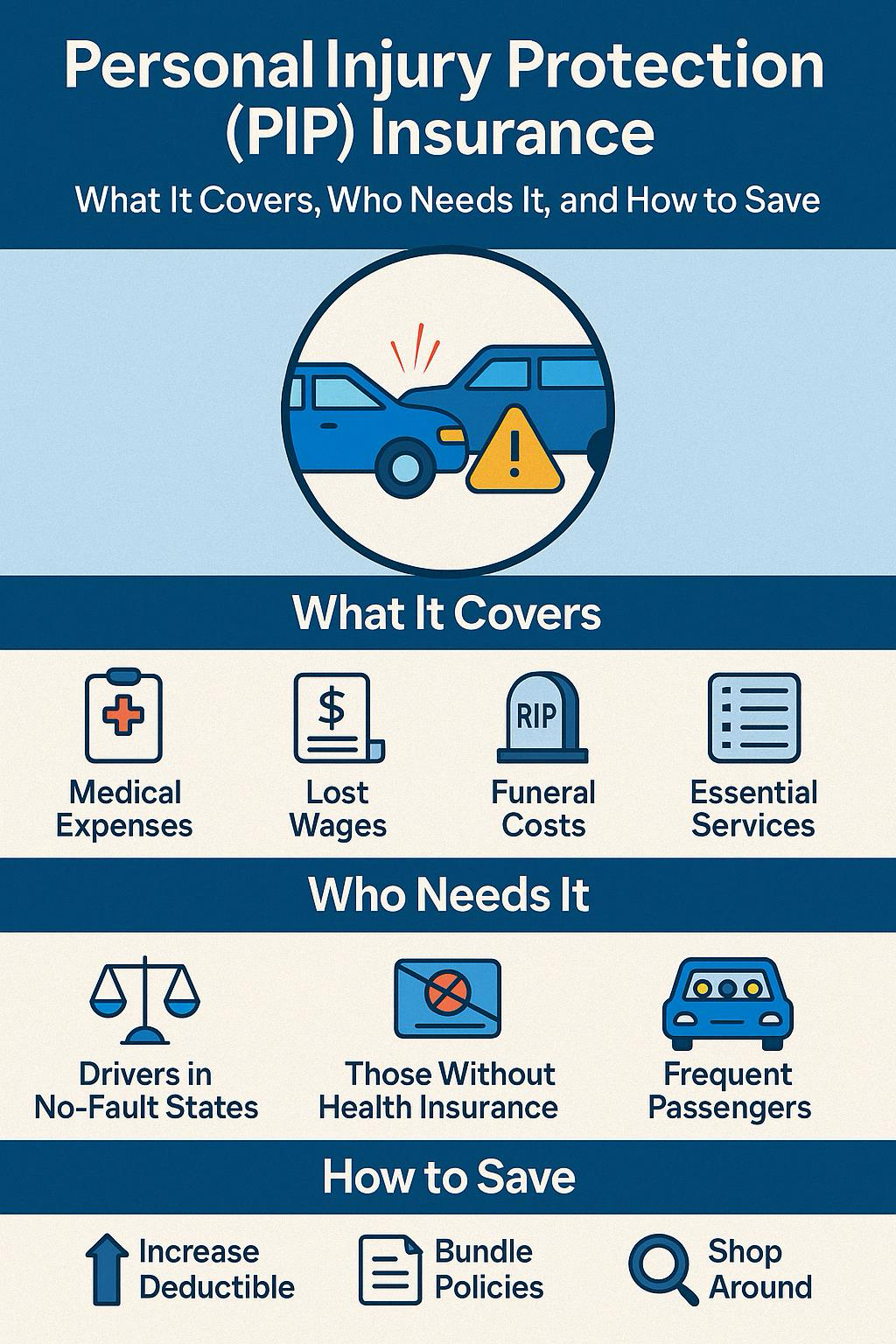

Personal Injury Protection (PIP) is a type of car insurance that covers medical expenses and lost wages for you and your passengers after an accident, regardless of who was at fault. PIP is often referred to as “no-fault insurance”, because it pays out even if you caused the accident.

PIP covers more than just doctor or hospital bills. It can include:

- Medical and surgical expenses

- Lost income if you’re unable to work

- Rehabilitation and physical therapy

- Essential services (e.g., childcare or housekeeping if you're injured)

- Funeral expenses (in some policies)

This makes it especially valuable if you lack sufficient health insurance or can’t afford to miss work after an injury.

Is PIP Insurance Required by Law?

Yes in some states. PIP is mandatory in most no-fault states, and optional or unavailable in others.

States Where PIP Is Required (as of 2024):

- Florida

- New York

- New Jersey

- Michigan

- Pennsylvania

- Hawaii

- Kansas

- Kentucky (can reject it)

- Massachusetts

- Minnesota

- North Dakota

- Utah

States Where PIP Is Optional:

- Texas

- Washington

- Arkansas

- Delaware

- Oregon

If you live in a required or no-fault state, you must carry at least the minimum PIP coverage as mandated by law.

What Does PIP Not Cover?

- Damage to your car (collision coverage handles that)

- Injuries to others not in your vehicle (covered by liability)

- Property damage

- Pain and suffering claims (requires additional legal action)

For broader coverage, some drivers pair PIP with MedPay (Medical Payments Coverage), which also pays for medical expenses, but without wage loss or service benefits.

How Much PIP Coverage Do You Need?

It depends on:

- Your state minimum requirements

- Your health insurance plan (is it high-deductible? limited coverage?)

- Your income (do you want wage replacement?)

- How often you drive with passengers

Common limits range from $2,500 to $50,000 or more. In states like New York and Michigan, default coverage can be much higher due to higher costs of living and care.

How Much Does PIP Insurance Cost?

PIP coverage is generally affordable, especially when bundled with a full auto policy. Average annual costs range from $50 to $200++, depending on:

| Factor | Effect on Cost |

| State regulations | Higher in mandatory no-fault states |

| Coverage limits | Higher limits = higher premiums |

| Deductibles (if applicable) | Higher deductibles = lower premiums |

| Health insurance status | Some states allow coordination with health plans |

| Driving history | Clean record = lower rates |

| Insurer pricing | Rates vary significantly by carrier |

Why You Need PIP Insurance

Here’s why PIP is valuable even in states where it’s optional:

- Fast Medical Reimbursement: No waiting for claim investigations.

- Covers Gaps in Health Insurance: Great for high-deductible health plans.

- Pays for Lost Wages: Essential if you're temporarily disabled from working.

- Covers Non-Medical Services: Like childcare or home cleaning assistance.

- Peace of Mind: You're covered no matter who caused the accident.

Ways to Save on Personal Injury Protection

- Coordinate With Health Insurance: Some states allow you to make health insurance your primary medical payer, which can reduce your PIP cost.

- Opt for Higher Deductibles (if allowed): Not all states offer PIP deductibles, but where they do, this can reduce premiums.

- Select Lower Limits (if risk is low): Choose the minimum required if you have good health and disability coverage.

- Bundle Your Policies: Combine PIP with other coverage (home, renters) to get multi-policy discounts.

- Shop Around: Compare quotes rates for PIP vary widely between insurers and states.

- Maintain a Clean Driving Record: Avoid accidents and citations that affect your overall premium.

PIP vs. MedPay vs. Liability: What’s the Difference?

| Feature | PIP | MedPay | Bodily Injury Liability |

| Fault Required? | No (pays regardless of fault) | No | Yes (only pays for others' injuries) |

| Medical Bills | ✅ Yes | ✅ Yes | ❌ No |

| Lost Wages | ✅ Yes | ❌ No | ❌ No |

| Funeral Expenses | ✅ Sometimes | ✅ Sometimes | ✅ For others |

| Pain & Suffering | ❌ No (requires lawsuit) | ❌ No | ✅ If you are liable |

Final Thoughts

PIP is more than just a legal checkbox in no-fault states it’s a financial shield that protects your health, income, and independence after a car accident. While not required in every state, it’s often a smart addition to your auto policy, especially if you don’t have robust health or disability insurance.

With affordable rates and flexible coverage limits, PIP can help you recover faster without draining your savings or depending on other drivers’ insurance.