Auto Insurance News

1. Introduction

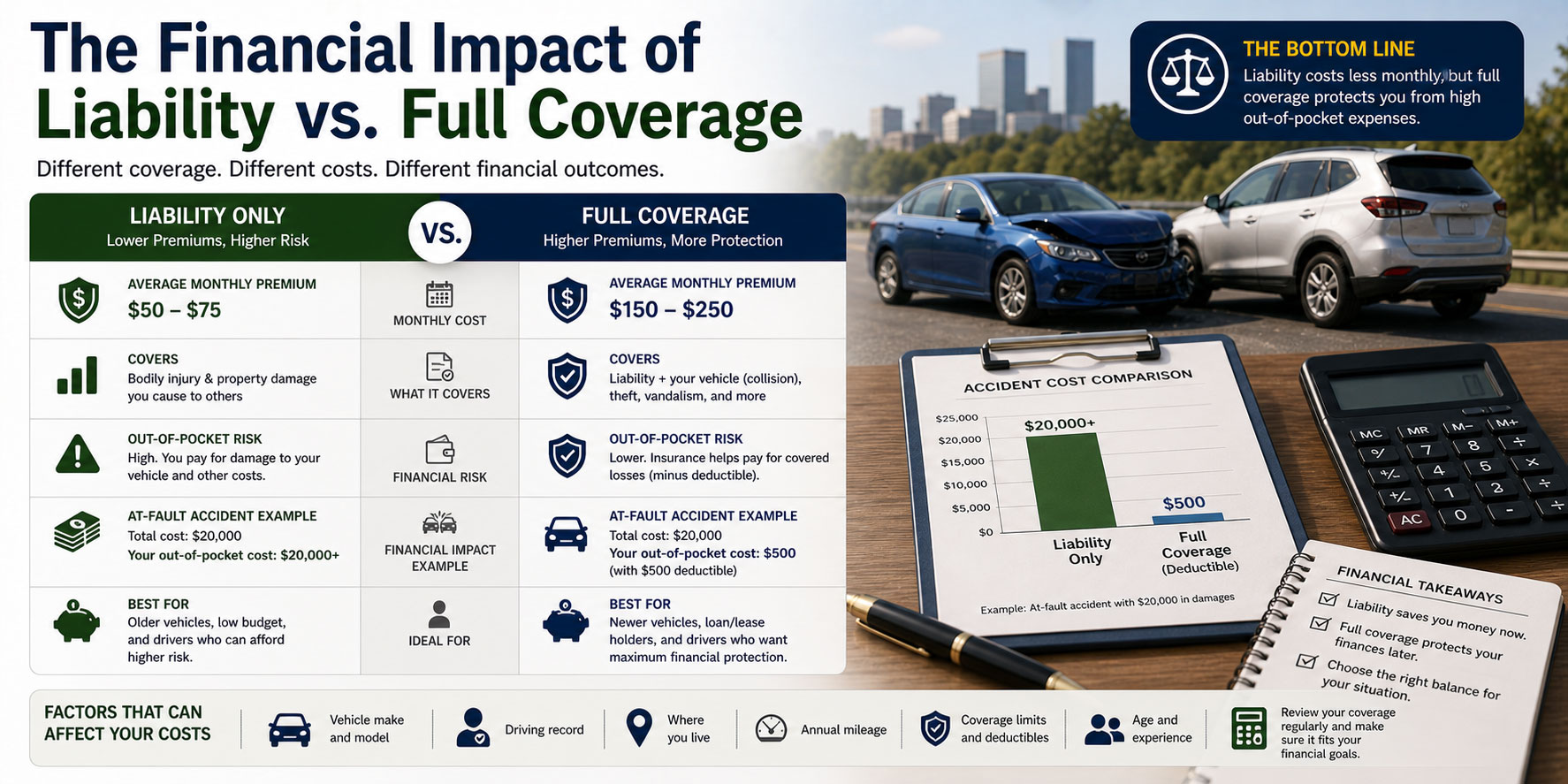

For many Americans, a vehicle is their most valuable asset after their home. Protecting that asset requires a choice between liability-only and full coverage insurance. Liability is the “minimum” required by law to keep your license valid. Full coverage is the financial safety net that protects you if your car is stolen, crashed, or damaged by weather.

Most drivers think about insurance only after an accident happens, but the most important work is done during the shopping phase. Understanding the price-to-protection ratio helps you avoid being “insurance poor” while ensuring you aren’t one accident away from financial ruin. You can use autoinsuranceplans.com to compare quotes from insurance companies and see exactly how these different coverage levels impact your bottom line.

2. What This Service Includes

Before looking at the price, you must understand exactly what you are getting for your money.

Defining Liability Protection

Liability is broken down into “per person” and “per accident” limits. For example, a 25/50/25 policy means the company will pay up to 25,000 dollars for one person’s injuries, 50,000 dollars for everyone’s injuries in the accident, and 25,000 dollars for property damage. This coverage is strictly for the people you hurt. It pays for their surgery, their pain and suffering, and the repairs to their vehicle.

Defining Full Coverage Protection

Full coverage is a broader protection package. It includes everything in liability plus two key additions:

- Collision Insurance: This is for when your car is in motion. It pays to fix your car if you hit a pole, a building, or another vehicle.

- Comprehensive Insurance: This is for “stationary” or “unpredictable” events. It covers theft, vandalism, fire, flood, and hitting animals.

What isn’t included

Standard insurance does not cover the contents of your car. If someone breaks your window and steals your laptop, the insurance will pay for the window (if you have comprehensive), but it will not pay for the laptop. You also are not covered for “intentional acts.” If you crash your car on purpose, the insurance company will deny the claim and may report you for fraud.

3. Average Cost Overview

The cost difference between these two options is usually the difference between “basic legal” and “financial peace of mind.”

Typical price ranges

- Liability Only (Minimums): $500 to $900 per year.

- Full Coverage (Older Car): $1,200 to $1,800 per year.

- Full Coverage (New SUV/Truck): $2,000 to $3,500 per year.

Simple cost summary table

| Service Option | Typical Annual Price | Price for High-Risk Drivers |

| Liability Only | $600 to $1,100 | $1,500 to $2,500 |

| Liability + Comp | $800 to $1,400 | $1,800 to $2,800 |

| Full Coverage | $1,500 to $2,600 | $3,500 to $6,000 |

The primary driver of the high end of the range is usually the driver’s age and location. A 19-year-old male in a major city will pay significantly more for full coverage than a 45-year-old female in a rural suburb.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

If you want to understand why your quote is high or low, you need to look at these specific variables.

- Deductible: This is your “buy-in” for a claim. Increasing your deductible from 500 to 1,000 dollars can drop your full coverage cost by as much as 20 percent.

- Amount of Coverage: Higher liability limits (like 250/500/100) are recommended for anyone with a house or significant savings. It costs more than the minimum but prevents your assets from being seized.

- Window Replacement: Some states offer “full glass” as an add-on. This is helpful because a modern windshield with sensors can cost over 1,000 dollars to replace.

- At-Fault History: Accidents stay on your record for three to five years. During this time, you will pay a higher “risk” premium for both liability and collision coverage.

- No-Fault State Laws: If you are in a state where insurance is “no-fault,” the price of your policy will be higher because the insurer is required to pay for your medical bills regardless of who caused the crash.

- Annual Mileage: If you drive 20,000 miles a year, you are statistically more likely to have a collision than someone who drives 5,000 miles. Low-mileage drivers get lower rates.

9. Ways to Save Money Without Cutting Corners

Budgeting for insurance doesn’t have to be a nightmare if you use the right tools.

Required versus optional coverage

Check your policy for “Towing and Labor” or “Emergency Roadside.” Many people pay for these through their insurance even though they already have them through their cell phone provider or a new car warranty. Removing these duplicates can save you 50 to 100 dollars a year. Also, consider “Usage-Based Insurance” (UBI) if you are a safe driver. This is where a device in your car tracks your driving and gives you a discount for being safe.

Comparing multiple quotes

Quote comparison is the only way to beat the “loyalty penalty.” Many insurance companies raise rates for existing customers while offering low rates to new ones. By comparing quotes every 12 months at autoinsuranceplans.com, you ensure that you are always on the winning side of the price equation.

11. Common Mistakes and Red Flags

A major mistake is letting your insurance “lapse.” If you don’t pay your bill and the policy is canceled, you will be considered “uninsured.” When you try to buy a new policy, even for liability only, the company will charge you a much higher rate because you had a gap in coverage.

A red flag to watch out for is a policy that uses “Actual Cash Value” for parts. Some cheap policies will only pay for used or refurbished parts after a collision. If you want brand-new manufacturer parts, you need to ensure that is specified in your “Full Coverage” agreement.

12. Frequently Asked Questions (FAQ)

Is liability insurance enough?

Liability is only “enough” if you are comfortable losing your car entirely. If your car is crashed or stolen and you only have liability, you receive zero dollars from the insurance company.

How fast can I get a quote?

You can usually get an accurate quote in five to ten minutes if you have your Vehicle Identification Number (VIN) and driving history ready.

Does full coverage protect me from a hit-and-run?

Yes. If someone hits your parked car and flees, your collision or uninsured motorist property damage coverage will pay for the repairs.

Is my car’s color a cost factor?

No. This is a common myth. Insurance companies do not care if your car is red, black, or silver. They care about the make, model, and engine size.

What is a “High Risk” driver?

A high-risk driver is someone with multiple tickets, a DUI, or a history of causing accidents. These drivers often have to use “non-standard” insurance companies.

Should I choose a 500 or 1,000 dollar deductible?

Choose the 1,000 dollar deductible only if you actually have 1,000 dollars in a savings account. If you don’t, you won’t be able to get your car out of the shop after a wreck.