Auto Insurance News

Introduction

If you are ever hit by a driver who has no insurance, you could be left paying for your own medical bills, lost wages, and vehicle repairs. That is exactly the situation that uninsured motorist coverage is designed to prevent. This type of coverage, often called UM coverage, steps in when the at-fault driver cannot pay because they have no insurance policy in force.

More drivers are on the road without insurance than many people realize. According to the Insurance Research Council, roughly 1 in 8 drivers in the United States is uninsured at any given time. In some states, that number is closer to 1 in 4. Whether you are driving in a busy urban area or on a rural highway, the risk is real and the financial consequences of an uninsured accident can be severe.

This guide explains exactly what uninsured motorist coverage includes, what it typically costs, and how to decide how much you need. You can use autoinsuranceplans.com to compare quotes from multiple insurance companies and find the right level of protection for your situation.

What Uninsured Motorist Coverage Includes

Core Definition

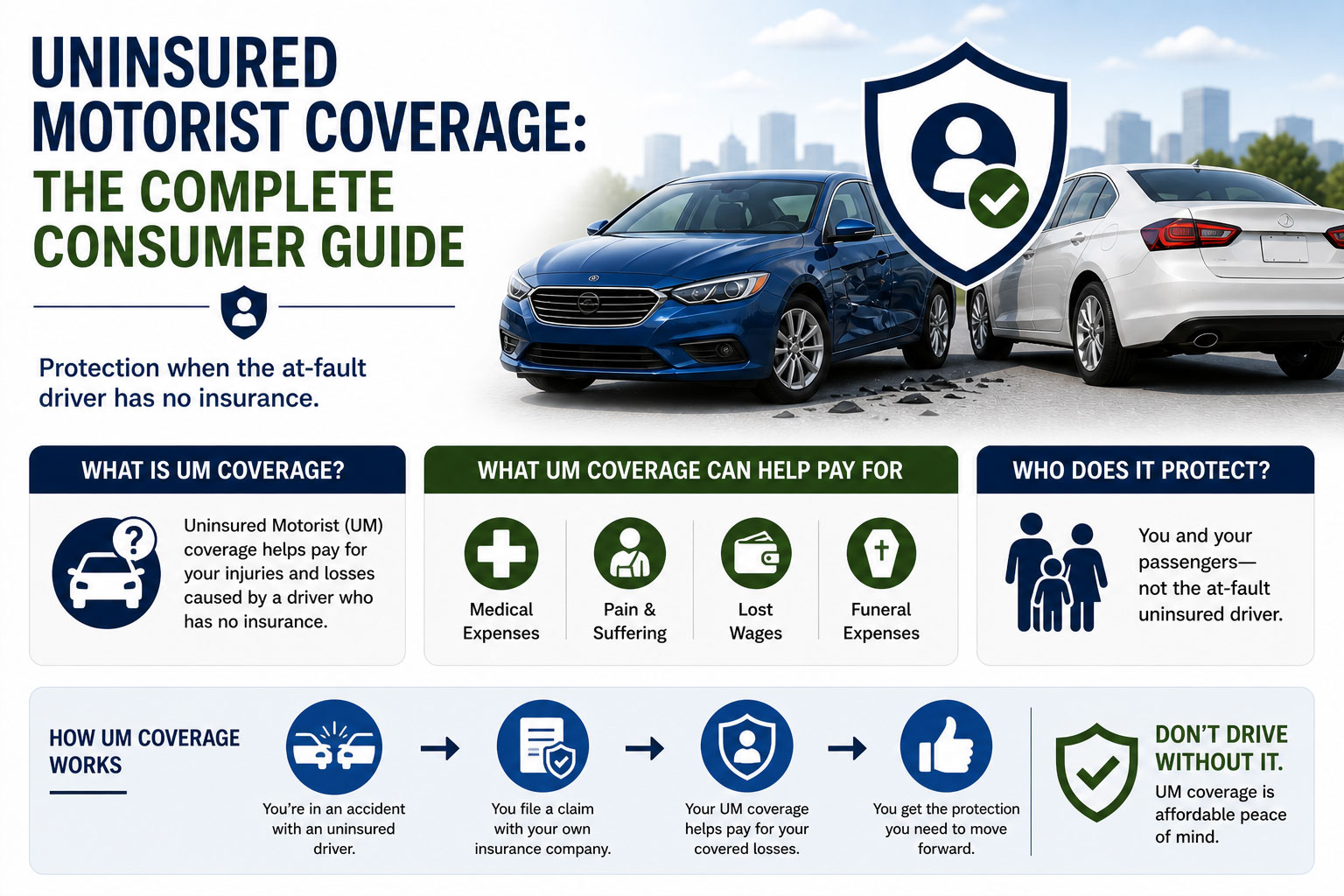

Uninsured motorist coverage pays for your injuries and sometimes your vehicle damage when a driver who carries no liability insurance hits you. It is not about your own fault. It activates specifically because the other driver is at fault but has no coverage to pay for your losses.

What Is Typically Included

Most uninsured motorist policies include two distinct components that are sometimes purchased together or separately depending on your state:

- Uninsured Motorist Bodily Injury (UMBI): This covers medical expenses, lost wages, pain and suffering, and funeral expenses for you and your passengers when injured by an uninsured driver.

- Uninsured Motorist Property Damage (UMPD): This covers repairs to your vehicle when an uninsured driver damages it. Some states require this, others treat it as optional. It is sometimes subject to a deductible.

- Hit-and-run accidents are also typically covered under UM coverage, meaning a driver who flees the scene is treated as an uninsured driver for purposes of your claim.

- Passengers in your vehicle are generally covered under your UM policy.

- Family members living in your household are usually covered when riding in other vehicles or even as pedestrians.

What Is Usually Not Included

- Damage to your own vehicle from a collision you caused. That requires collision coverage.

- Medical expenses if you caused the accident. That is handled by your own health insurance or medical payments coverage.

- Damage to other people’s property. That is covered under your liability insurance.

- Some states do not require or offer UMPD. In those states, collision coverage or comprehensive coverage handles your vehicle damage.

Average Cost Overview

Uninsured motorist coverage is one of the more affordable additions to an auto insurance policy. The exact cost depends on your state, your coverage limits, your driving history, and the insurer you choose. The ranges below reflect typical annual costs added to a standard policy.

Coverage Option Typical Annual Price Range

Basic UM/UIM (25/50K limits) $50 to $90 per year

Mid-Range UM/UIM (50/100K limits) $90 to $160 per year

High Coverage UM/UIM (100/300K limits) $160 to $280 per year

UMPD (Property Damage Add-On) $20 to $60 per year

Full UM Package (BI + PD combined) $80 to $320 per year

Drivers with clean records and modest vehicles in low-cost states such as Maine, Iowa, or Wisconsin tend to fall at the lower end of these ranges. Drivers in high-uninsured states such as Florida, Michigan, or Mississippi, or those with prior claims, tend to pay more.

In most cases, uninsured motorist coverage adds less than $15 to $25 per month to your total premium, making it one of the most cost-effective protections available given the risk it offsets.

Ready to compare your options? Visit www.autoinsuranceplans.com to get quotes from multiple trusted insurance companies and find the right uninsured motorist protection at a competitive price.

Key Cost Factors

What Drives Your Premium Up or Down

- State requirements: About 22 states plus Washington D.C. require drivers to carry uninsured motorist coverage. In mandatory states, base rates are built into every standard policy. In optional states, pricing is more competitive.

- Coverage limits: Higher limits cost more. A 100/300 policy (meaning $100,000 per person and $300,000 per accident) costs more than a 25/50 policy, but provides far more protection for serious injuries.

- Deductible on UMPD: Some states allow a deductible on the property damage portion of UM coverage. Choosing a higher deductible, such as $500 or $1,000, lowers your premium.

- Your driving record: A history of at-fault accidents or violations raises your overall premium, including UM rates, since insurers factor overall risk into every component.

- Vehicle value: For UMPD specifically, higher-value vehicles may carry a slightly higher rate to reflect the cost of repairs.

- Your location: Urban zip codes with higher accident rates and higher concentrations of uninsured drivers typically produce higher UM premiums than rural areas.

- Stacking options: Some states allow you to stack UM coverage across multiple vehicles on your policy. For example, if you have two cars with $100,000 of UM each, stacking means you can access $200,000 in coverage for one accident. Stacked policies cost more but offer significantly higher protection.

- Insurance company: Rates for identical coverage can vary by 20 percent or more between insurers. This is why comparing multiple quotes is essential.

Ways to Save Money Without Cutting Corners

Required vs. Optional Coverage

In states where UM coverage is mandatory, you cannot waive it legally. In states where it is optional, you can decline it, but doing so exposes you to significant financial risk. Before waiving this coverage to save money, consider that even a minor injury accident can generate tens of thousands of dollars in medical bills. The cost of carrying UM coverage is almost always lower than the cost of a single uninsured accident.

UMPD, on the other hand, may be more optional in nature if you already carry collision coverage on your vehicle. Collision coverage handles your vehicle damage regardless of fault. If you have both, you may be paying twice for similar protection. Ask your agent whether you need UMPD if you already carry collision.

Practical Tips for Lowering Your Cost

- Compare multiple quotes: Use autoinsuranceplans.com to get side-by-side pricing from multiple insurers. The same limits from different companies can vary considerably.

- Bundle your policies: Many insurers offer discounts when you combine auto and home or renters insurance with the same company.

- Maintain a clean driving record: Your record affects every part of your premium. Safe driving lowers your overall risk profile over time.

- Choose your deductible carefully: On UMPD, a higher deductible reduces your premium. On UMBI, there is typically no deductible, so the tradeoff does not apply.

- Ask about loyalty or safe driver discounts: Many insurers offer reduced rates to long-term customers or drivers who complete a defensive driving course.

- Review your policy annually: Your needs change. As your vehicle ages or your financial situation changes, you may need to adjust your coverage levels.

Common Mistakes and Red Flags

- Assuming everyone on the road is insured: Even in states with mandatory insurance laws, enforcement is limited and a large share of drivers carry no policy.

- Choosing limits that are too low: State minimum UM limits are often far below the actual cost of a serious injury accident. Choosing $25,000 in UMBI when a hospital stay can cost $50,000 or more leaves you underprotected.

- Waiving UM to save a few dollars: The annual premium for UM coverage is modest. Skipping it to save $5 to $15 per month is a significant risk trade-off that rarely makes financial sense.

- Not understanding hit-and-run coverage: Many drivers do not realize that UM coverage applies to hit-and-run accidents. Failing to file a UM claim after a hit-and-run means leaving money on the table.

- Failing to report promptly: UM claims generally must be reported to your insurer quickly. Waiting too long can complicate or even invalidate your claim.

- Not knowing your state’s stacking rules: Stacking can dramatically increase your available coverage. Drivers who are eligible but never asked about stacking may be significantly underprotected.

- Confusing UM with UIM: Uninsured motorist covers drivers with no insurance. Underinsured motorist, or UIM, covers drivers who have some insurance but not enough. These are related but distinct coverages, and you may need both.

Frequently Asked Questions

Is uninsured motorist coverage required in my state?

It depends on where you live. As of 2025, roughly 22 states and Washington D.C. require at least some form of UM coverage. States including Virginia, Maryland, New York, and Illinois mandate it. States like California, Texas, and Florida offer it as an optional add-on. Check your state’s department of insurance website or ask your agent for current requirements.

How much uninsured motorist coverage do I need?

Most financial advisors suggest matching your UM limits to your bodily injury liability limits. If you carry 100/300 liability, carry 100/300 in UM as well. This ensures you are as protected when the other driver is uninsured as you are when you are at fault.

What happens if the uninsured driver has some assets?

You can file a UM claim with your insurer and then pursue the at-fault driver in civil court for any amount not covered. However, drivers without insurance are often judgment-proof, meaning they have little to collect even if you win a lawsuit. Your UM coverage is usually the faster and more reliable recovery option.

Does UM cover me if I am a pedestrian or cyclist?

Generally yes. Most UM policies extend to you and family members in your household even when you are not in a vehicle, including situations where an uninsured driver hits you while you are walking or riding a bicycle.

Will filing a UM claim raise my premium?

In most cases, a UM claim does not raise your premium the same way an at-fault collision does, since you are the victim. However, policies and state laws vary. Ask your insurer about their specific claims handling approach before filing.

Can I stack UM coverage across multiple vehicles?

This depends on your state and your policy. Stacking is allowed in many states and can significantly increase the total coverage available to you. Ask your insurer about stacked versus non-stacked options when you purchase or renew.

What is the difference between UM and collision coverage?

Collision coverage pays for your vehicle repairs regardless of fault, including accidents you cause. UM property damage coverage specifically covers your vehicle when an uninsured driver hits you. If you have collision, you may not need UMPD. If you do not have collision, UMPD fills that gap for uninsured-driver scenarios.

What if the uninsured driver is a family member?

Most policies exclude coverage for accidents involving household family members driving your vehicle. If a family member who is not listed on your policy is driving and causes an accident, your UM coverage would not apply in that situation. Speak with your agent about how household drivers affect your policy.

Ready to find the right uninsured motorist coverage? Use www.autoinsuranceplans.com to compare quotes from trusted insurance companies and get protected with confidence.