Auto Insurance News

1. Introduction

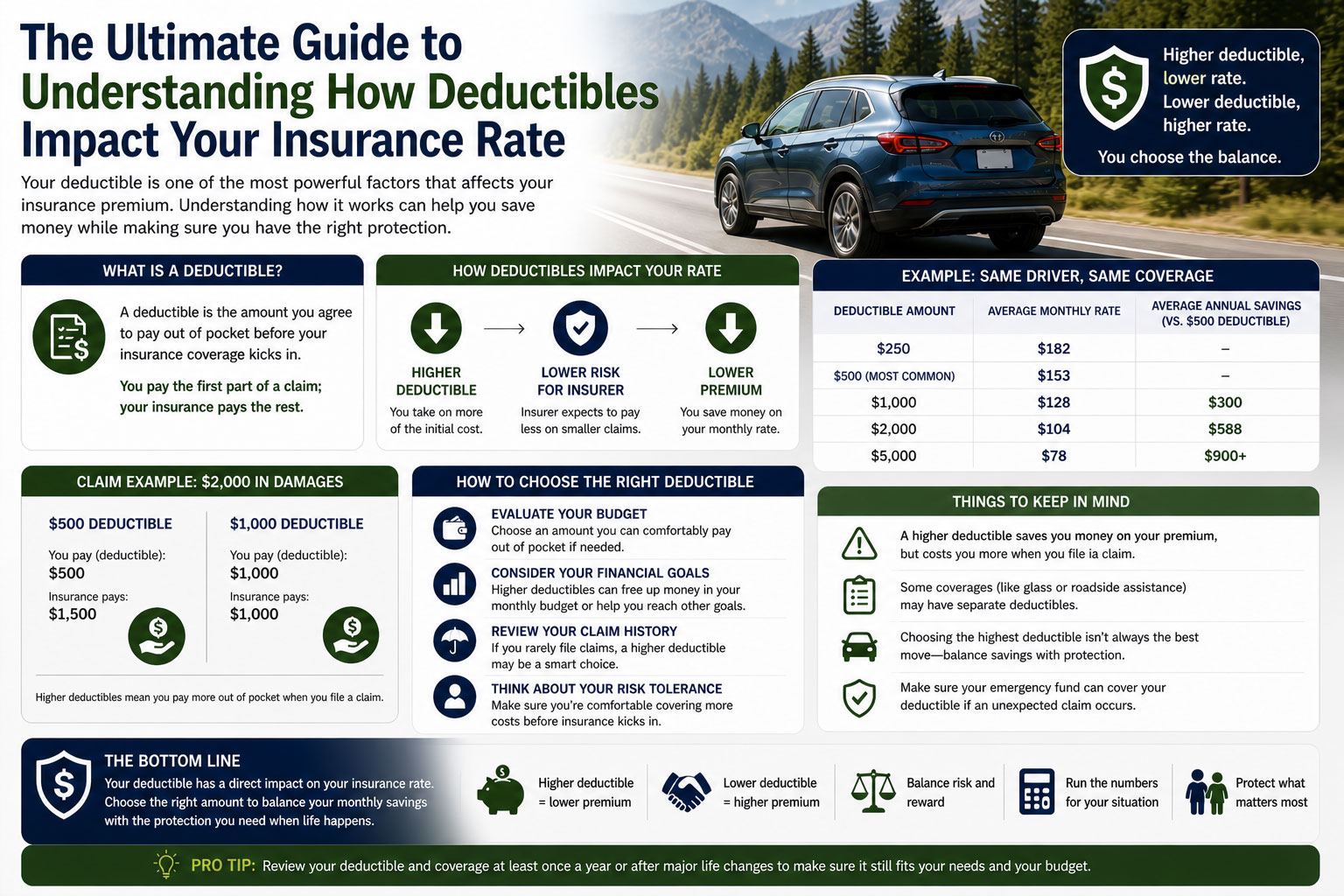

When you sign up for an auto insurance policy, one of the most important decisions you will make is choosing your deductible. A deductible is the specific amount of money you agree to pay out of your own pocket before your insurance coverage begins to pay for a claim. This choice directly influences your monthly or annual premium costs. Most drivers encounter this decision when purchasing collision or comprehensive coverage, as these are the areas where deductibles are most common.

Understanding how this number affects your financial health is crucial for any vehicle owner. If you choose a high deductible, you will likely see a lower monthly bill, but you must be prepared to pay more in the event of an accident. Conversely, a low deductible means higher monthly payments but less financial strain after a sudden mishap. To see exactly how these numbers play out for your specific vehicle and location, readers can use autoinsuranceplans.com to compare quotes from insurance companies. This tool allows you to toggle different deductible amounts so you can visualize the impact on your rates in real time.

2. What This Service Includes

In the context of auto insurance, the “service” being discussed is the deductible management feature of your policy. This is not an add on but a core component of how your insurance contract is structured.

Defining the Deductible in Simple Terms

A deductible is a form of risk sharing. By choosing a deductible, you are telling the insurance company that you are willing to take on a certain amount of the financial risk. In exchange for you taking on that first 500 dollars or 1,000 dollars of a repair bill, the insurance company agrees to lower the amount they charge you for the policy.

What is Typically Included

Most standard auto insurance policies apply deductibles to two main types of coverage. The first is Collision Coverage, which pays for damage to your car if you hit another vehicle or an object like a fence. The second is Comprehensive Coverage, which covers non collision events such as theft, vandalism, fire, or damage from falling trees. When you select your deductible service, you are setting the threshold for these specific protections. You usually have the option to set different deductible amounts for each type of coverage depending on your needs.

What is Usually Extra or Not Included

It is important to understand that deductibles do not typically apply to Liability Insurance. If you are at fault in an accident and cause injury to another person or damage to their property, your insurance usually pays for those costs starting from the first dollar, up to your policy limit. You do not have to pay a deductible to “activate” your liability coverage.

Additionally, some specialized coverages like Roadside Assistance, Towing and Labor, or Gap Insurance usually do not have deductibles. Some states also offer “Full Glass” coverage as an extra feature. In this case, you might pay a small additional premium to have your windshield replaced with a zero dollar deductible, meaning the insurance company pays the full cost regardless of your standard comprehensive deductible.

3. Average Cost Overview

The relationship between your deductible and your insurance rate is inverse. As one goes up, the other goes down. While exact numbers vary by state and driver history, there are clear patterns in how insurance companies price these options.

Typical Price Ranges

In the United States, the most common deductible amounts are 250, 500, and 1,000 dollars. Choosing a 1,000 dollar deductible instead of a 250 dollar deductible can often save a driver between 15 percent and 30 percent on their annual premium.

- Typical low price range: Drivers who choose a high deductible (1,000 to 2,000 dollars) will see the lowest premiums.

- Typical average price range: This is usually found with a 500 dollar deductible, which is the industry standard for most moderate income households.

- Typical high price range: Drivers who want the security of a low deductible (100 to 250 dollars) or a zero dollar deductible will pay the highest premiums.

Deductible Impact on Annual Premium Table

| Deductible Option | Typical Annual Premium Savings | Estimated Monthly Cost |

| Low Deductible ($100 – $250) | 0% (Baseline high cost) | $150 to $250 |

| Standard Deductible ($500) | 10% to 15% Savings | $120 to $180 |

| High Deductible ($1,000) | 20% to 30% Savings | $90 to $140 |

| Premium Deductible ($2,000+) | 35% to 45% Savings | $70 to $110 |

What Drives the Low Versus High Ends

The primary driver of the cost difference is the insurance company’s administrative expense and risk. Small claims, such as a 400 dollar bumper scratch, are very common. If you have a 250 dollar deductible, the insurance company has to process a claim and pay out 150 dollars. If you have a 500 dollar deductible, they pay nothing and avoid the administrative cost of the claim entirely. This is why the premium drops so significantly when you move from a low to a high deductible. Your personal driving record and the value of your car also play a role. A high value luxury car will have higher premiums regardless of the deductible, but the percentage of savings remains similar.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

Several variables determine how much your deductible will ultimately change your rate. Understanding these can help you fine tune your policy.

- Deductible Amount: This is the most direct factor. The jump from 500 dollars to 1,000 dollars usually yields the most significant savings for the average driver.

- Amount of Coverage: If you have high limits on your collision and comprehensive coverage, the impact of the deductible is more pronounced.

- Window Replacement: As mentioned earlier, some policies treat glass differently. If you live in an area with high rates of cracked windshields, opting for a lower comprehensive deductible or a glass endorsement might increase your rate but save you money in the long run.

- At Fault History: If you have multiple at fault accidents on your record, your base premium is already high. In this situation, raising your deductible can be a strategic way to bring your monthly costs back down to a manageable level.

- No Fault State Regulations: In states with no fault insurance laws, personal injury protection (PIP) is required. PIP often comes with its own separate deductible, which is distinct from your vehicle repair deductible. This can add an extra layer of cost complexity.

- Vehicle Age: For older vehicles that have a lower market value, it often makes sense to carry a high deductible. If your car is only worth 3,000 dollars, paying a high premium for a 100 dollar deductible is mathematically inefficient.

5. Ways to Save Money Without Cutting Corners

You do not have to sacrifice quality protection to get a better price on your auto insurance. Here are practical ways to manage your costs.

Required vs. Optional Coverage

In almost every state, liability insurance is required by law, but collision and comprehensive are optional unless you are financing or leasing your car. If your vehicle is paid off and has a low resale value, you might save the most money by dropping these coverages entirely. However, if you choose to keep them, raising the deductible is the safest way to lower the price without losing the safety net for a total loss.

Comparing Multiple Quotes

Insurance companies use different algorithms to calculate how much a deductible change affects a rate. Company A might give you a 10 percent discount for a 1,000 dollar deductible, while Company B might give you a 25 percent discount for the exact same change. This is why it is essential to look at multiple providers. By checking different options, you can find the insurer that rewards your willingness to take on a higher deductible the most.

6. Common Mistakes and Red Flags

One of the most frequent mistakes is choosing a deductible that you cannot actually afford to pay on short notice. If your car is in the shop and you need it to get to work, but you cannot come up with the 1,000 dollars to cover your high deductible, your insurance policy has failed to provide its primary benefit.

Another red flag is failing to adjust your deductible as your financial situation or car’s value changes. Many people set a deductible when they buy a new car and never look at it again. As the car ages, that low deductible becomes less and less valuable. Conversely, as you save more money in an emergency fund, you may be able to handle a higher deductible and save hundreds of dollars a year in premiums.

Finally, be wary of “vanishing deductibles” that sound too good to be true. While these can be a great feature where the company lowers your deductible for every year of safe driving, they often come with an additional fee that might be higher than the actual value of the benefit.

7. Frequently Asked Questions (FAQ)

How much can I really save by doubling my deductible?

On average, moving from a 500 dollar to a 1,000 dollar deductible can save you between 15 percent and 30 percent on your collision and comprehensive premiums.

When do I have to pay my deductible?

You typically pay it directly to the repair shop after an accident. If your car is totaled, the insurance company will subtract the deductible from the check they send you.

Is it better to have a low or high deductible?

It depends on your savings. If you have 1,000 dollars in a savings account specifically for car repairs, a high deductible is usually better. If you live paycheck to paycheck, a low deductible is safer.

Does my deductible affect my safety on the road?

Indirectly, yes. Drivers with high deductibles are often more cautious because they know they have more skin in the game if an accident occurs.

Can I change my deductible in the middle of a policy term?

Yes, most insurance companies allow you to adjust your deductible at any time. Your premium will be pro rated for the remainder of the term.

Does a higher deductible affect the quality of repairs?

No. The quality of repairs is determined by the shop you choose and the insurance company’s standards, not by the amount of your deductible.

What happens if the accident wasn’t my fault?

If the other driver is at fault and has insurance, their company should pay for your repairs without a deductible. If you use your own insurance first, your company will try to get your deductible back from the other insurer through a process called subrogation.

Is a 0 dollar deductible worth it?

Rarely. The premium for a 0 dollar deductible is usually so high that you end up paying the equivalent of a 500 dollar deductible in extra premiums within just a year or two.