Auto Insurance News

Introduction

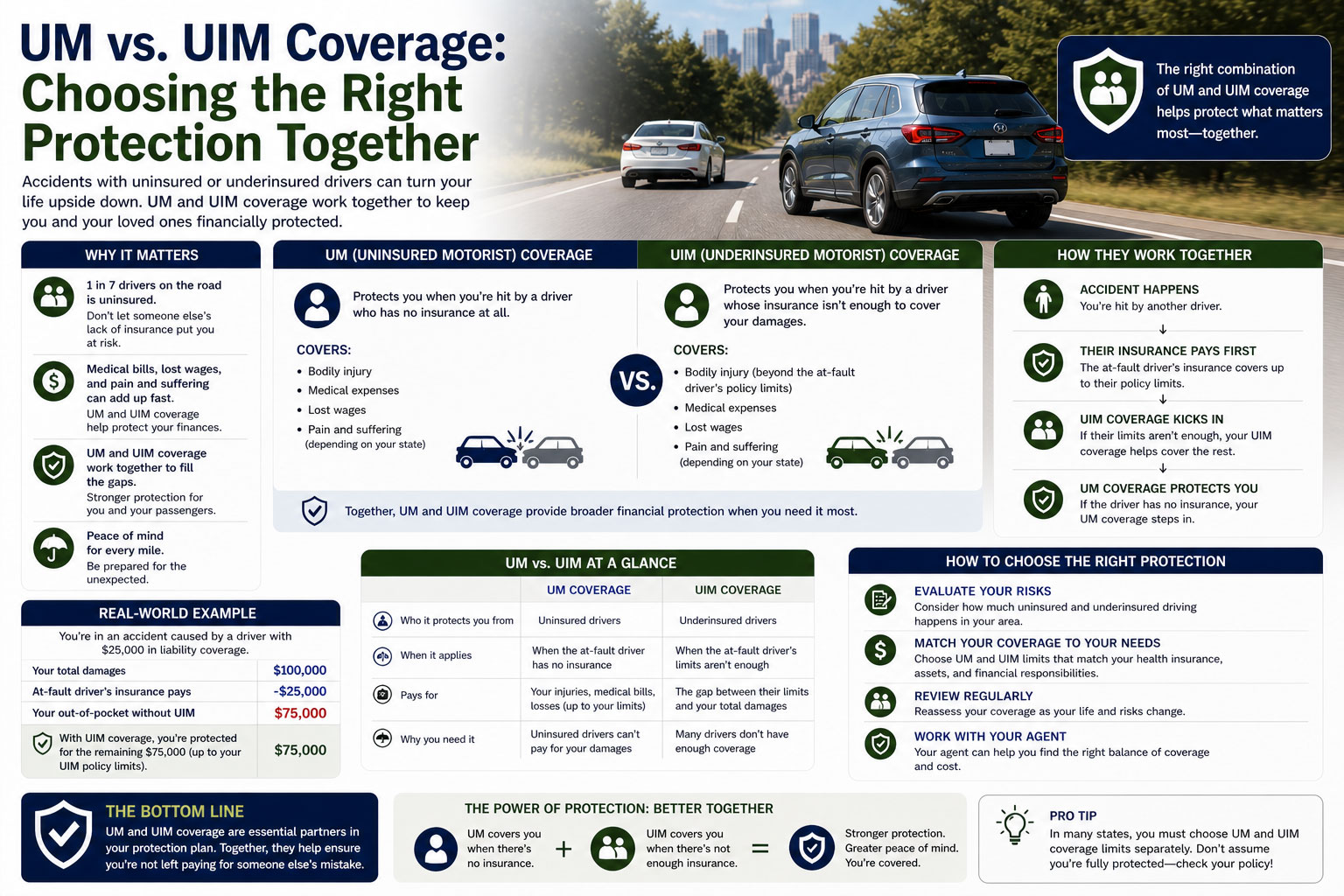

Two of the most misunderstood components of an auto insurance policy are uninsured motorist coverage and underinsured motorist coverage. Most drivers have heard of them, many have them on their policy, and yet very few understand exactly how they work together or why the combination matters so much.

This guide takes a direct look at UM and UIM coverage side by side. It explains the difference between the two, when each one applies, how they are priced together, and how to decide on the right limits for your specific situation. Whether you are buying a new policy or reviewing an existing one, this is the information you need to make a confident decision.

You can compare quotes and coverage options from multiple insurance companies right now at autoinsuranceplans.com.

What UM and UIM Coverage Include

Uninsured Motorist Coverage (UM)

Uninsured motorist coverage applies when you are in an accident caused by a driver who carries no auto insurance. It also applies in hit-and-run situations where the at-fault driver cannot be identified. UM typically covers:

- UM Bodily Injury (UMBI): Medical bills, lost wages, rehabilitation, pain and suffering, and funeral expenses for you and passengers in your vehicle.

- UM Property Damage (UMPD): Repair or replacement of your vehicle when an uninsured driver damages it. Not available in all states.

Underinsured Motorist Coverage (UIM)

Underinsured motorist coverage applies when the at-fault driver has insurance but their policy limits are insufficient to cover your actual losses. It bridges the gap between what they can pay and what you are owed:

- UIM Bodily Injury (UIMBI): Covers the shortfall between the at-fault driver’s liability payout and your actual medical and wage loss expenses.

- UIM Property Damage (UIMPD): Less common, but available in some states to cover vehicle repair gaps when the at-fault driver’s property coverage is insufficient.

What Both Exclude

- Accidents you cause. Your liability insurance handles the other party’s costs when you are at fault.

- Damage from natural events such as flooding, hail, or falling objects. That falls under comprehensive coverage.

- Intentional acts or criminal activity by the policyholder.

- Commercial or business use accidents may have different rules depending on the policy.

Combined Cost Overview

When purchased together, UM and UIM coverage often come as a bundled product at a combined rate. Separate pricing is less common but available from some insurers. The ranges below reflect combined annual costs for both coverages:

Coverage Option Typical Annual Price Range

Basic UM + UIM Bundle (25/50K) $80 to $160 per year

Mid-Range UM + UIM Bundle (50/100K) $150 to $270 per year

High Coverage UM + UIM Bundle (100/300K) $270 to $480 per year

Premium UM + UIM with UMPD/UIMPD $310 to $580 per year

Stacked UM + UIM (where available) $400 to $700+ per year

These are annual additions to your base premium, not total policy costs. The majority of drivers who choose mid-range limits will add approximately $12 to $22 per month to their overall premium for complete UM and UIM protection. In most states, this is one of the highest-value additions you can make to a policy.

Get a personalized quote that includes UM and UIM coverage options. Visit www.autoinsuranceplans.com to compare rates from trusted insurers side by side.

Key Cost Factors

How UM and UIM Pricing Is Determined

- State regulations: States that mandate both UM and UIM tend to have built-in base rates that all carriers must offer. Optional states have more competitive pricing but also more variation between companies.

- Coverage limits chosen: The single biggest pricing factor. Doubling your limits does not usually double your premium, but it does increase cost proportionally.

- Stacking election: Stacked UM/UIM policies multiply your coverage by the number of vehicles insured and carry a higher premium. Non-stacked policies cost less but provide lower maximum coverage.

- At-fault vs. no-fault state: In no-fault states, your own personal injury protection (PIP) coverage pays first regardless of who caused the accident. UM and UIM interact differently with PIP, and pricing reflects that structure.

- Driving record and claims history: Your overall risk profile affects every premium component. Maintaining a clean record keeps all coverage costs lower.

- Local risk environment: Zip codes with higher uninsured driver rates, more dense traffic, or higher medical costs produce higher UM and UIM premiums.

- Vehicle characteristics: For UMPD and UIMPD, the value and repair cost of your vehicle affects pricing. For bodily injury components, vehicle characteristics matter less.

- Insurer pricing models: Two insurers offering identical coverage can price it quite differently. Shopping the market is the only reliable way to find the best rate.

Ways to Save Money Without Cutting Corners

Understand What Is Required and What Is Optional

Whether UM or UIM is required depends on your state. In mandatory states, both must be included unless you formally reject them in writing, which some states allow. In optional states, you choose whether to add them. The cost of adding both is typically modest compared to the financial exposure of going without them.

UMPD and UIMPD are more discretionary, especially if you carry collision coverage. Collision covers your vehicle regardless of who is at fault, which means it already handles damage from uninsured or underinsured drivers on the property side. If you do not carry collision, adding UMPD fills an important gap.

Practical Savings Strategies

- Shop multiple carriers: Use autoinsuranceplans.com to compare combined UM and UIM pricing across companies. Rates vary significantly and shopping takes minutes.

- Purchase UM and UIM together: Bundled pricing is usually more economical than buying each separately.

- Match your limits to your overall coverage structure: If you carry 100/300 liability, carry the same in UM/UIM. Lower UM/UIM limits create a gap in your protection without meaningful savings.

- Consider raising other deductibles instead: If you need to cut premium costs, raising your collision deductible to $1,000 is often a better tradeoff than reducing UM/UIM limits.

- Eliminate UMPD if you have collision: This is one area where trimming overlap may make sense without sacrificing meaningful protection.

- Maintain continuous coverage: Lapses in coverage can raise your premium when you reinstate. Continuous coverage signals lower risk to insurers.

Common Mistakes and Red Flags

- Having UM but not UIM or vice versa: These coverages address different scenarios and most drivers need both. Having one without the other leaves you exposed.

- Carrying state minimum limits only: Minimum limits are designed to satisfy legal requirements, not to cover serious injury accidents. They are often insufficient for real-world scenarios.

- Not knowing whether your state is at-fault or no-fault: In no-fault states, your own PIP coverage handles immediate medical expenses regardless of fault. UM and UIM still matter for serious injuries that exceed PIP limits, but the interaction is different. Know your state’s rules.

- Accepting a quick settlement from the other driver’s insurer: If you settle with the at-fault driver’s insurer before notifying your own carrier of a potential UIM claim, you may forfeit your UIM rights. Always contact your insurer before settling.

- Not filing a UM claim after a hit-and-run: Hit-and-run accidents are covered by UM. Many drivers do not realize this and simply absorb the loss.

- Buying a policy without reviewing UM/UIM limits annually: Your financial situation, vehicle value, and risk profile change. What was sufficient three years ago may not be today.

- Assuming higher liability limits make UM/UIM less important: High liability limits protect other people when you cause an accident. UM/UIM protect you when someone else causes one. They serve different purposes and both are needed.

Frequently Asked Questions

Do I need both UM and UIM, or just one?

Most drivers benefit from carrying both. UM covers the scenario where the at-fault driver has no insurance. UIM covers the far more common scenario where the at-fault driver has minimal insurance that falls short of your actual damages. Carrying only one leaves a significant gap.

How do I know if my state requires UM or UIM?

The most reliable sources are your state’s department of insurance website and your insurance agent. Requirements change periodically. As of 2025, about 22 states mandate some form of UM coverage, and a slightly smaller number require UIM. Some states allow written rejection of mandatory coverages.

Can my limits for UM and UIM be different?

This depends on your state. In many states, UM and UIM limits must be equal. In others, you can choose different levels. If your state allows it and you want to reduce cost slightly, you might explore whether a combination of higher UM and lower UIM makes sense given local uninsured driver rates.

What does it mean to stack UM/UIM coverage?

Stacking allows you to multiply your coverage by the number of vehicles on your policy. If you have three cars each with $100,000 of UMBI, stacked coverage provides up to $300,000 per accident. Stacking is not allowed in all states but provides significant additional protection where it is available.

How does a hit-and-run work with UM coverage?

If an unidentified driver causes an accident and flees, most UM policies treat that driver as uninsured, allowing you to file a UM claim. Some states require physical contact between vehicles to allow a UM hit-and-run claim. Others accept witness testimony. Know your state’s specific rule.

What happens if both UM and UIM apply to the same accident?

This is uncommon because UM applies when there is no insurance and UIM applies when there is some. They typically do not overlap. If an accident involved an uninsured driver and you are claiming both vehicle and injury losses, you might file UMBI for injuries and UMPD for property, but both fall under the UM umbrella, not UIM.

How does a no-fault state affect my UM and UIM coverage?

In no-fault states, your own personal injury protection pays for medical expenses first regardless of who caused the accident. UM and UIM still matter for serious injuries that exceed your PIP limits and for property damage claims. The threshold for when you can pursue a tort claim against an at-fault driver varies by state.

What should I do immediately after an accident with an uninsured or underinsured driver?

Document the scene thoroughly with photos. Get the other driver’s information even if they claim to have no insurance. File a police report. Contact your own insurer promptly, even before speaking with the other driver’s insurer. Do not accept any settlement from the other party’s insurer without consulting your own carrier first.

Is UM/UIM more important in some states than others?

Yes. States with high uninsured driver rates, such as Mississippi, Michigan, Tennessee, New Mexico, and Washington, present greater UM risk. States where drivers commonly carry only minimum limits present greater UIM risk. Checking your state’s uninsured driver rate is a useful guide for choosing limits.

Can I get a quote for UM and UIM coverage before committing to a policy?

Absolutely. Most insurers provide quotes that include UM and UIM as line items. You can compare the cost of different limit levels side by side. Use autoinsuranceplans.com to get quotes from multiple companies and review exactly how UM and UIM affect your total premium.

Ready to compare UM and UIM coverage options? Use www.autoinsuranceplans.com to get quotes from trusted auto insurance companies and choose the protection that gives you confidence on every drive.