Auto Insurance News

Introduction

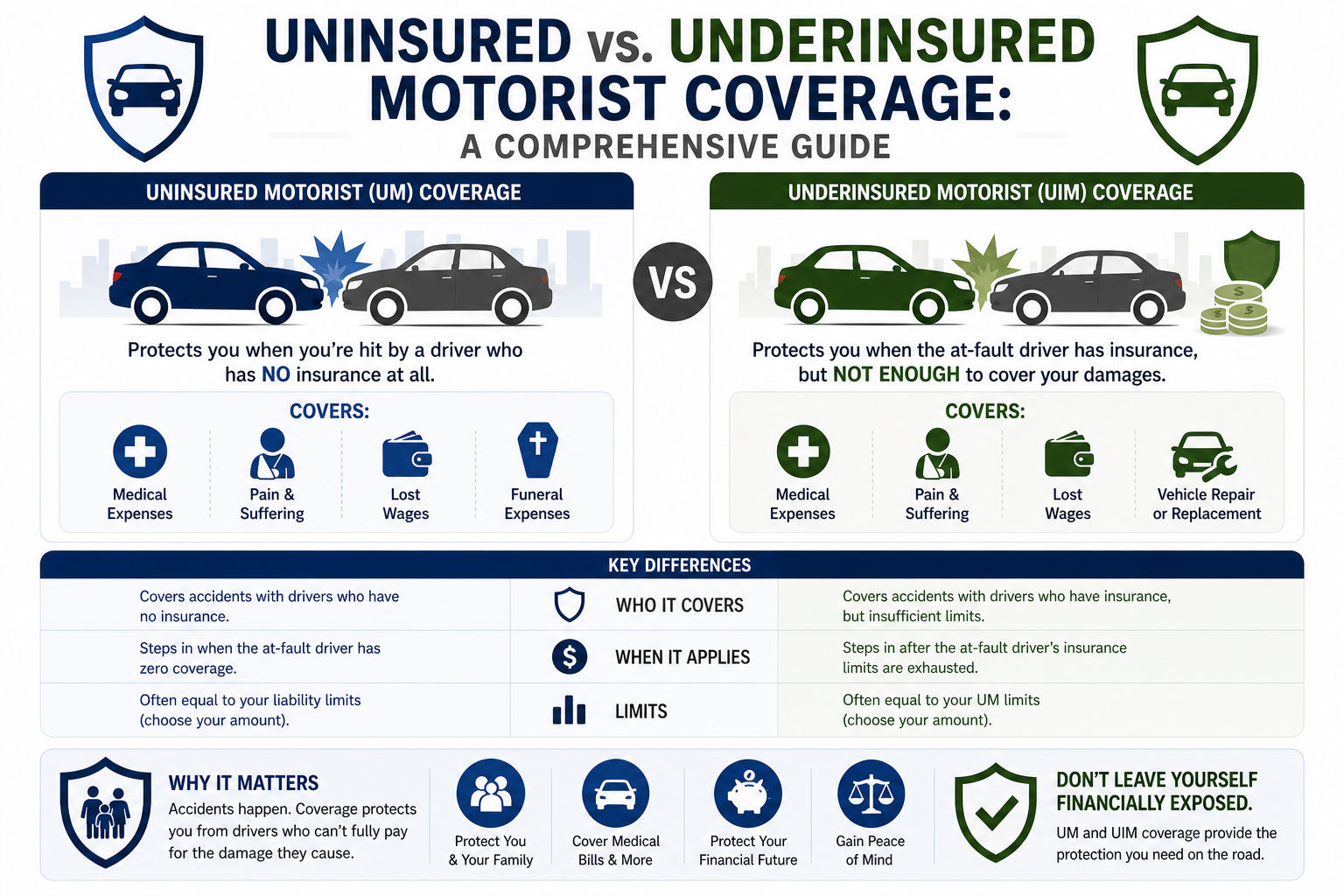

When you get behind the wheel, you assume that other drivers are as responsible as you are. Unfortunately, millions of Americans drive without any insurance at all, while millions more carry only the bare minimum required by law. If you are involved in an accident with one of these drivers, you could be left facing massive medical bills and repair costs on your own. This is where Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage become essential.

People usually need this service to provide a financial safety net that their standard liability policy does not offer. While liability insurance pays for the damage you cause to others, UM and UIM coverage protect you, your passengers, and your vehicle from the negligence of others. In many states, this coverage is optional, but it is often the most valuable part of a policy when the unthinkable happens. To ensure you are getting the best protection for your budget, you can use autoinsuranceplans.com to compare quotes from insurance companies. Seeing these options side by side helps you understand how a small monthly addition to your premium can save you from financial ruin.

What This Service Includes

Understanding the mechanics of these coverages is the first step toward securing your financial future. These services are designed to step into the shoes of the at-fault driver’s insurance company when that company either does not exist or does not have enough money to pay your claims.

Defining the Service in Simple Terms

Uninsured Motorist (UM) coverage applies when you are hit by a driver who has no auto insurance at all. It also typically applies in hit and run situations where the other driver cannot be identified. Underinsured Motorist (UIM) coverage applies when the other driver has insurance, but their policy limits are too low to cover the full extent of your injuries or property damage. For example, if you have 100,000 dollars in medical bills but the person who hit you only has 25,000 dollars in coverage, your UIM policy would help pay the remaining 75,000 dollars.

What is Typically Included

There are two primary components to this coverage: Bodily Injury and Property Damage.

Uninsured Motorist Bodily Injury (UMBI) covers medical expenses for you and your passengers. It also covers lost wages if you are unable to work after the accident. More importantly, it can cover non-economic damages such as pain and suffering, which your own health insurance will never pay for.

Uninsured Motorist Property Damage (UMPD) pays for repairs to your vehicle. In some states, this also covers personal property inside the car that was damaged during the collision. This is particularly useful if you do not carry collision insurance on an older vehicle but still want protection if an uninsured driver hits you.

What is Usually Extra or Not Included

While these coverages are robust, they do not cover everything. They generally do not cover intentional acts, such as if someone deliberately rams your car. They also do not cover your own medical bills if you were the one at fault for the accident.

In some states, UMPD is not available if you already have collision coverage, or it may have a specific deductible that is different from your standard deductible. Additionally, “stacking” coverage, which allows you to combine limits across multiple vehicles on your policy, is often an extra feature that carries a higher premium. You must specifically request stacked coverage in states where it is allowed if you want that extra layer of protection.

Average Cost Overview

The cost of UM and UIM coverage is relatively low compared to the high level of protection it provides. Because the insurance company is only paying out after other options are exhausted, the premiums remain affordable for most drivers.

Typical Cost Ranges in U.S. Dollars

The pricing for these coverages is usually calculated as a percentage of your total premium or as a flat fee per vehicle. For a standard policy in 2026, you can expect the following ranges:

- Typical low price range: 40 to 75 dollars per year.

- Typical average price range: 100 to 250 dollars per year.

- Typical high price range: 300 to 600 dollars per year.

Service Option and Typical Price Table

| Coverage Option | Typical Annual Price Range |

| Basic (State Minimum UM/UIM) | $45 to $95 |

| Mid-range (100/300 Limits) | $110 to $220 |

| Premium (High Limits + Stacking) | $250 to $550 |

What Drives the Low Versus High Ends

The low end of the price range is typically found in states with very low rates of uninsured drivers or in rural areas where accidents are less frequent. Drivers with excellent credit scores and clean driving records also see lower costs.

The high end of the range is driven by living in urban areas with high crime or high accident rates. Furthermore, if you live in a state like Mississippi or Florida, where nearly one in four drivers may be uninsured, insurance companies charge more because the statistical likelihood of you filing a UM claim is much higher. Choosing to “stack” your coverage will also push you into the higher price brackets.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

Key Cost Factors

Several specific variables will dictate exactly how much you pay for your UM and UIM protection. Understanding these factors allows you to adjust your policy to fit your budget.

- Amount of Coverage: The most obvious factor is the limit you choose. If you choose 25,000 dollars in coverage, it will be cheap. If you choose 250,000 dollars, the price will increase. Experts recommend matching your UM/UIM limits to your own liability limits.

- Deductible: While Bodily Injury coverage often has no deductible, Property Damage (UMPD) usually does. Choosing a 500 dollar deductible instead of a 250 dollar deductible will lower your premium.

- Stacking versus Non-Stacking: If you have three cars and choose stacked coverage, you are essentially buying three times the protection. This is a significant driver of cost but provides massive security.

- At-Fault History: Even though UM coverage is for accidents caused by others, your general risk profile affects your entire policy. If you have a history of accidents, your base premium will be higher, which often scales the cost of add-ons.

- Location (State and Zip Code): Insurance is regulated at the state level. Some states mandate this coverage, while others make it optional. Your specific zip code matters because it determines the density of uninsured motorists in your immediate area.

- Number of Vehicles: Most companies charge a fee per vehicle for UM/UIM coverage. Adding a teenager or an additional car to your policy will naturally increase the total cost of these protections.

Ways to Save Money Without Cutting Corners

You do not have to sacrifice safety to save money on your auto insurance. There are practical ways to keep your premiums low while maintaining high UM/UIM limits.

Understand Required vs. Optional Coverage

In some states, UM coverage is mandatory. In others, you can reject it in writing. However, before you reject it to save 10 dollars a month, consider the cost of a single ER visit in 2026. A better way to save is to check if your health insurance already covers auto related injuries. If you have a top tier health plan with a low deductible, you might feel comfortable carrying lower UMBI limits, though health insurance will not cover your lost wages or pain and suffering.

Comparing Multiple Quotes

The price of UM/UIM coverage varies wildly between companies. One insurer might see your city as high risk, while another might have more favorable data. By using a tool like autoinsuranceplans.com, you can see these price differences in real time. Shopping around every six to twelve months ensures that you are not paying an “inflation tax” on your policy. Many companies offer discounts for new customers that can offset the cost of higher coverage limits.

Common Mistakes and Red Flags

One of the most frequent mistakes is assuming that “Full Coverage” automatically includes UM and UIM. In many states, full coverage only refers to liability, collision, and comprehensive. You must often specifically add UM and UIM to the policy.

Another red flag is a policy that only offers “Uninsured” but not “Underinsured” coverage. If you are hit by someone with a 15,000 dollar limit and your surgery costs 50,000 dollars, a policy that only has UM will not help you because the other driver technically had insurance.

Finally, do not make the mistake of choosing lower UM/UIM limits than your liability limits. If you think 100,000 dollars is the minimum you need to protect yourself if you hit someone else, it should also be the minimum you have to protect yourself if someone hits you.

Frequently Asked Questions (FAQ)

Does UM coverage pay for hit and runs?

In most states, yes. Uninsured Motorist Bodily Injury usually covers hit and run accidents. However, some states require physical contact with the other vehicle for the claim to be valid, and some states do not allow hit and run claims under the Property Damage portion.

How long does it take to settle a UM claim?

UM claims can take anywhere from a few weeks to several months. Because you are dealing with your own insurance company, the process is often smoother than dealing with a third party, but they will still conduct a full investigation into the fault of the accident.

Is the quality of coverage the same across all companies?

The legal requirements are the same, but the claims experience differs. Higher rated companies often have better mobile apps and faster payout times. It is worth checking consumer reviews before choosing the cheapest option.

Will my rates go up if I file a UM claim?

In many states, insurance companies are prohibited from raising your rates for a claim where you were not at fault. Since UM/UIM claims by definition involve another at-fault driver, your rates are generally safe, but you should verify your state’s specific laws.

Do I need this if I have health insurance?

Health insurance is great for medical bills, but it does not cover everything. It will not pay for your car repairs, it will not pay for your lost income, and it will not provide compensation for permanent disability or pain. UM/UIM fills these critical gaps.

Can I add UM coverage at any time?

Yes. You can call your agent or go online to update your policy at any time. The change is usually effective immediately once you pay the pro-rated difference in premium.

What is the difference between stacked and unstacked?

Stacked coverage lets you combine limits. If you have two cars with 50,000 dollars in UM coverage each, stacking them gives you 100,000 dollars of protection. Unstacked means you are limited to 50,000 dollars regardless of how many cars you own.

Is UM/UIM coverage mandatory in the U.S.?

It depends on the state. About twenty states require it by law. In other states, insurers are required to offer it to you, but you have the right to decline it in writing.