Auto Insurance News

Introduction

Every time you pull out of your driveway, you share the road with millions of other drivers. Most of them carry auto insurance, but a surprising number do not, and many others carry only the bare legal minimum. If one of those drivers hits you and causes serious damage or injury, you could be left paying out of pocket for costs that were not your fault.

That is exactly the problem that uninsured motorist coverage (UM) and underinsured motorist coverage (UIM) are designed to solve. These two coverages protect you when the driver responsible for an accident either has no insurance at all or does not have enough to cover your losses.

Understanding how UM and UIM work, what they cover, and what they cost is one of the smartest steps you can take as a vehicle owner. You can use autoinsuranceplans.com to compare quotes from multiple insurance companies and find the right level of protection for your situation.

What This Service Includes

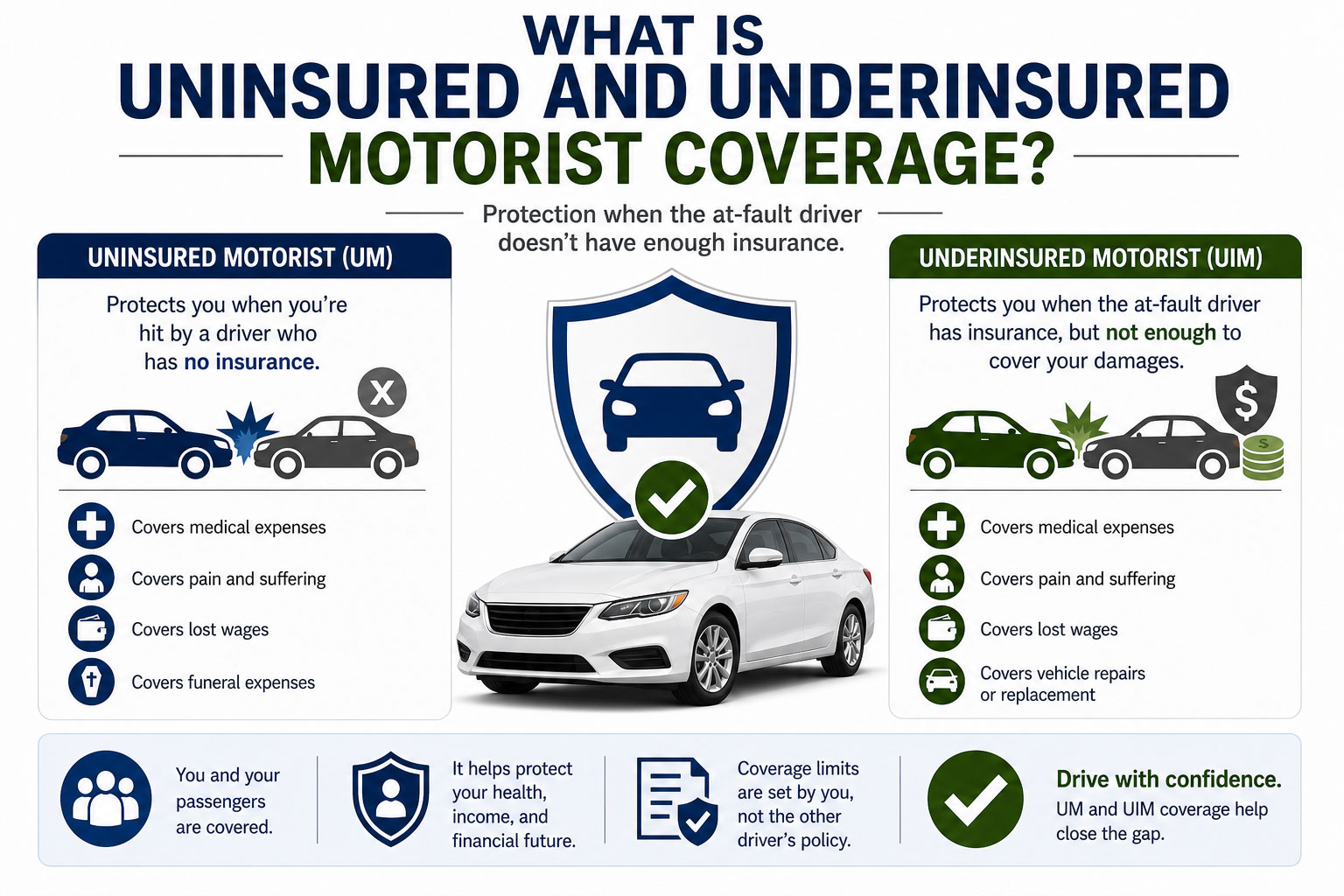

Uninsured Motorist Coverage (UM)

Uninsured motorist coverage steps in when you are hit by a driver who carries zero auto insurance. It also typically applies in hit-and-run accidents where the responsible driver flees and cannot be identified.

UM coverage generally includes two components:

Uninsured Motorist Bodily Injury (UMBI): Pays for medical expenses, lost wages, pain and suffering, and funeral costs for you and your passengers when an uninsured driver causes the accident.

Uninsured Motorist Property Damage (UMPD): Covers damage to your vehicle caused by an uninsured driver. This is separate from collision coverage and often carries a lower deductible.

Underinsured Motorist Coverage (UIM)

Underinsured motorist coverage applies when the at-fault driver has insurance, but their policy limits are too low to cover all your losses. For example, if your medical bills total $80,000 and the other driver carries only $25,000 in bodily injury liability, UIM pays the gap up to your policy limit.

Underinsured Motorist Bodily Injury (UIMBI): Covers your medical bills, lost income, and pain and suffering beyond what the at-fault driver’s policy pays.

Underinsured Motorist Property Damage (UIMPD): Available in some states, this covers vehicle damage beyond what the at-fault driver’s property damage liability covers.

What Is Usually Extra or Not Included

UM and UIM do not cover your own liability to others. They do not replace comprehensive or collision coverage for non-accident damage such as theft, weather, or vandalism. Coverage for rental cars during repairs is typically a separate add-on. Medical payments coverage (MedPay) or personal injury protection (PIP) overlap with UM bodily injury in some states and are handled differently depending on your state’s laws.

Average Cost Overview

UM and UIM are among the most affordable coverages available, especially considering the financial protection they provide.

| Coverage Option | Typical Annual Cost |

| Basic UM/UIM (state minimum limits) | $50 to $100 per year |

| Mid-range UM/UIM ($100k/$300k limits) | $100 to $200 per year |

| High UM/UIM ($250k/$500k limits) | $200 to $400 per year |

| Stacked UM/UIM (multi-vehicle) | $250 to $500 per year |

These figures represent averages across U.S. states. Your actual premium will vary based on your location, driving history, vehicle, and the insurer you choose.

The low end of the range reflects drivers in states with high insurance compliance rates, clean driving records, and modest coverage limits. The high end reflects drivers in states with high rates of uninsured motorists, urban locations with dense traffic, or those choosing maximum coverage limits and stacking options.

Ready to compare your options? Use www.autoinsuranceplans.com to compare quotes from trusted auto insurance companies and find UM and UIM coverage that fits your budget and protects your family.

Key Cost Factors

- State requirements. Some states require UM/UIM coverage by law. Others make it optional or allow drivers to waive it in writing. Required coverage tends to be more uniformly priced.

- Coverage limits you choose. Higher bodily injury and property damage limits increase your premium. Limits are typically written as two numbers, such as $100,000 per person and $300,000 per accident.

- Stacked vs. non-stacked policies. In states that allow it, stacking lets you multiply your UM/UIM limits across multiple vehicles on one policy, which raises both protection and cost.

- Your driving record. A history of at-fault accidents or violations raises your overall premium, including UM/UIM.

- Your location. States like Florida, Mississippi, and Michigan have some of the highest uninsured driver rates in the country, which can influence local pricing.

- Your vehicle’s value. More expensive vehicles may prompt insurers to price UMPD slightly higher.

- Deductible on property damage. Some states allow a deductible on UMPD. Choosing a higher deductible lowers your premium.

Ways to Save Money Without Cutting Corners

Know what is required in your state. Many states mandate UMBI but make UMPD optional. Understanding exactly what the law requires helps you avoid paying for redundant coverage while staying legally protected.

Compare multiple quotes. UM/UIM pricing varies significantly between insurers for the same coverage levels. Getting at least three to five quotes through a comparison tool like autoinsuranceplans.com can reveal meaningful savings.

Bundle with your existing policy. Adding UM/UIM to a policy you already have with an insurer is almost always cheaper than buying it separately.

Raise your deductible on UMPD. If your state allows it, a higher property damage deductible on your uninsured motorist coverage can reduce your premium while keeping your bodily injury limits strong.

Ask about discounts. Safe driver discounts, multi-car discounts, and loyalty discounts can apply to your full policy, including UM/UIM components.

Common Mistakes and Red Flags

Waiving UM/UIM to save a few dollars. This is one of the most dangerous decisions a driver can make. The cost savings are small, but the financial exposure is enormous if you are ever hit by an uninsured driver.

Choosing limits that are too low. Many drivers select state minimum UM/UIM limits without realizing that a serious accident can quickly generate medical bills far exceeding those minimums. Match your UM/UIM limits to your overall liability limits whenever possible.

Assuming collision coverage replaces UM property damage. Collision covers your vehicle regardless of fault, but it often comes with a higher deductible. UMPD may cover your vehicle with no deductible in a hit-and-run, depending on your state.

Not understanding your state’s offset rules. Some states require that the at-fault driver’s insurance pay first, and UIM only covers the gap. Others allow your UIM to pay immediately. Misunderstanding this can cause delays in claim handling.

Forgetting passengers. Your UMBI coverage typically extends to passengers in your vehicle. Choosing low limits leaves everyone in your car exposed.

Frequently Asked Questions

Is uninsured motorist coverage required in every state? No. Roughly 20 states and Washington D.C. require UM coverage. The remaining states make it optional, though insurers are typically required to offer it. Check your state’s specific laws.

How many drivers on U.S. roads are uninsured? According to the Insurance Research Council, roughly one in eight U.S. drivers is uninsured. In some states, that number is closer to one in five.

Does UM coverage apply in a hit-and-run? In most states, yes. UMBI typically covers injuries from a hit-and-run accident. UMPD may require physical contact with the unidentified vehicle to apply, depending on your state.

What is the difference between UM and MedPay or PIP? MedPay and PIP cover your medical expenses regardless of fault and pay quickly. UM/UIM covers broader losses including lost wages and pain and suffering, but only when another driver is at fault and uninsured or underinsured.

Should my UM limits match my liability limits? Most insurance professionals recommend matching them. If you carry $100,000/$300,000 in liability, carrying the same in UM/UIM gives you consistent protection.

How do I file a UM/UIM claim? You file with your own insurance company, just as you would for a collision claim. Your insurer handles the process and may seek reimbursement from the at-fault driver.

Will filing a UM claim raise my rates? Policies vary. Filing a UM claim for a not-at-fault accident generally should not raise your rates, but practices differ by insurer and state. Ask your insurer about their specific policy.

What does “stacking” mean? Stacking allows you to combine UM/UIM limits across multiple vehicles. For example, if each car has a $100,000 UM limit and you stack two vehicles, you may have access to $200,000 in coverage for a single accident.