Auto Insurance News

Introduction

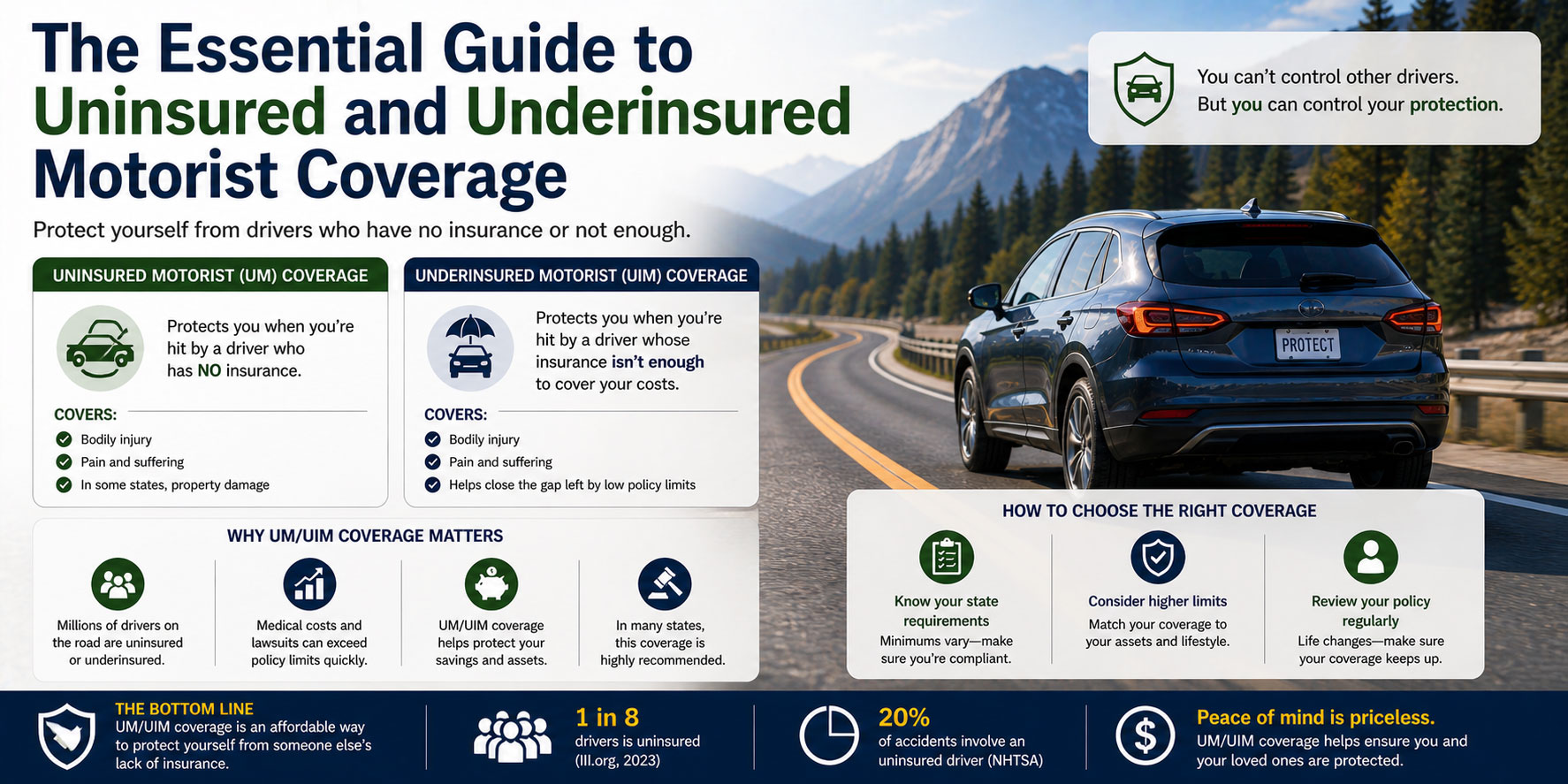

When you hit the road, you generally assume that other drivers are as responsible as you are. Unfortunately, millions of drivers in the United States operate vehicles without any insurance at all. Millions more carry only the bare minimum required by their state, which is often not enough to cover a serious accident. Uninsured and Underinsured Motorist coverage, often referred to as UM and UIM, is the specific part of an auto policy designed to protect you when the at-fault driver fails to meet their financial obligations.

People usually need this service when they realize that their own health insurance or standard liability coverage has significant gaps. Whether you are a daily commuter or an occasional driver, this protection ensures that you are not left paying out of pocket for someone else’s mistake. If you want to see how this coverage fits into your budget, you can use autoinsuranceplans.com to compare quotes from insurance companies. This comparison helps you secure a policy that balances cost with a high level of personal protection.

What This Service Includes

Understanding what you are buying is the first step toward becoming a savvy insurance consumer. UM and UIM are technically two separate coverages, though they are often bundled together for convenience.

Defining the Service in Simple Terms

Uninsured Motorist (UM) coverage kicks in if you are involved in an accident with a driver who has no insurance policy. It also applies in most hit and run situations where the other driver cannot be identified. Underinsured Motorist (UIM) coverage applies when the at-fault driver has insurance, but their policy limits are too low to cover the total cost of your medical bills or car repairs. Essentially, your own insurance company steps into the shoes of the other driver and pays the damages they owe you.

What is Typically Included

There are two primary branches of this coverage. The first is Bodily Injury (UMBI/UIMBI). This covers your medical expenses, lost wages, and compensation for pain and suffering. It protects you, your family members who live with you, and any passengers in your car at the time of the accident.

The second branch is Property Damage (UMPD). This pays for repairs to your vehicle. In some states, this is an alternative to collision coverage. If an uninsured driver hits your parked car or causes a multi-car pileup, UMPD ensures your vehicle is repaired without you having to rely on the other driver’s empty pockets.

What is Usually Extra or Not Included

Standard UM and UIM policies do not cover your own liability. If you are at fault in an accident, these coverages will not pay for the other person’s damages. Furthermore, “stacking” is often an optional feature. Stacking allows you to combine the UM/UIM limits of multiple vehicles on a single policy to create a larger pool of coverage. This is not allowed in every state and usually requires an extra premium.

This coverage also typically excludes non-car related incidents. While some policies might cover you if you are hit as a pedestrian or a cyclist, you must check the specific language of your policy. Rental car reimbursement and roadside assistance are also not included in a standard UM/UIM endorsement and must be purchased as separate add-ons.

Average Cost Overview

The cost of UM and UIM coverage is generally much lower than the cost of your primary liability or collision insurance. This is because the insurance company only pays out after it is proven that the other driver is uninsured or underinsured.

Typical Price Ranges

Prices for this coverage are influenced by the state you live in and the limits you choose. For a policy in 2026, you can expect the following annual price ranges:

- Typical low price range: 40 to 80 dollars per year.

- Typical average price range: 100 to 200 dollars per year.

- Typical high price range: 250 to 500 dollars per year.

Service Option Cost Table

| Service Option | Typical Price Range (Annual) |

| Basic (State Minimum Limits) | $40 to $90 |

| Mid-Range (100/300 Limits) | $120 to $230 |

| Premium (High Limits + Stacking) | $260 to $550 |

What Drives the Low Versus High Ends

The low end of the range is typically reserved for drivers in states with low percentages of uninsured motorists, such as Maine or New York. If you choose the lowest possible limits allowed by law, your costs will remain low.

The high end of the range is common in states like Mississippi or Florida, where the rate of uninsured drivers is statistically much higher. Additionally, choosing high limits to protect a high net worth or opting for “stacked” coverage will push your premium toward the high end of the scale. Your personal claims history and credit score also play a role in where you land within these brackets.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

Key Cost Factors

Several variables change the price of your UM and UIM coverage. Understanding these factors can help you adjust your policy to find the right price.

- Deductible: While Bodily Injury coverage often has no deductible, the Property Damage portion (UMPD) usually does. Choosing a higher deductible, such as 500 dollars instead of 250 dollars, can reduce the cost of this endorsement.

- Amount of Coverage: The higher your limits, the more you will pay. Most experts recommend matching your UM/UIM limits to your own Liability limits. If you carry 250,000 dollars in liability, you should carry 250,000 dollars in UM/UIM.

- Window Replacement: Some UMPD policies have specific rules about glass. If you want a policy that covers a windshield replacement with a zero dollar deductible after a hit and run, you might pay a slightly higher premium for that specific benefit.

- At-Fault History: Your history as a driver impacts the overall risk profile the insurance company assigns to you. If you have a history of accidents, even the add-on coverages like UM/UIM may be priced higher.

- No-Fault State Laws: In states with no-fault insurance laws, you are required to use your own Personal Injury Protection (PIP) first. This can sometimes make UM/UIM coverage cheaper because it only covers the “excess” damages that PIP does not reach.

- Location and Local References: Your zip code is a major factor. If you live in an area with high rates of uninsured motorists or high litigation costs, your premium will reflect that localized risk. Insurance companies use local data from the last three to five years to set these rates.

Ways to Save Money Without Cutting Corners

You do not have to settle for the first quote you see. There are strategic ways to keep your costs down while maintaining excellent protection.

Required versus Optional Coverage

The first step is to determine if UM/UIM is mandatory in your state. In about twenty states, it is required by law. In other states, it is optional. However, “optional” does not mean “unnecessary.” A better way to save is to evaluate your Property Damage coverage. If you already have a high quality collision policy, you might not need the UMPD portion of the coverage. Dropping the property damage part while keeping the bodily injury part can save you money without leaving you vulnerable to medical bankruptcy.

Comparing Multiple Quotes

Insurance companies update their rates frequently based on new data. A company that was the most expensive last year might be the most affordable this year. By using a comparison tool like autoinsuranceplans.com, you can see these shifts in real time. Comparing quotes every six months is the most effective way to ensure you are not paying more than the market rate for your UM and UIM protection.

Common Mistakes and Red Flags

One frequent mistake is assuming that health insurance is a complete substitute for UM coverage. Health insurance pays for your doctors, but it does not pay for your lost wages, your car repairs, or the pain and suffering associated with a permanent injury.

A major red flag is an insurance company that encourages you to “reject” UM/UIM coverage in writing without explaining the risks. Some low cost providers do this to make their initial quotes look lower. Always be wary of a policy that does not offer “Underinsured” protection alongside “Uninsured” protection. If you are hit by someone with 15,000 dollars in coverage and your bill is 50,000 dollars, you need the UIM portion to bridge that 35,000 dollar gap.

Frequently Asked Questions (FAQ)

Does UM coverage pay for hit and run accidents?

In most states, yes. Uninsured Motorist Bodily Injury usually covers hit and run accidents. However, some states require physical contact between the vehicles for a Property Damage claim to be valid.

How long does it take to settle a UM claim?

UM claims generally take the same amount of time as standard liability claims. Depending on the complexity of your injuries, it can range from a few weeks to several months.

Is the quality of the insurance company important for this coverage?

Quality is very important. Since you are filing a claim against your own company, you want a provider with a reputation for fair settlements and efficient customer service.

Will my rates go up if I file a UM claim?

In many states, insurance companies are prohibited from raising your rates for a claim where you were not at fault. However, you should check your local state regulations to be sure.

Does this coverage protect my passengers?

Yes. UM and UIM coverage typically extends to anyone who is legally riding in your vehicle at the time of the accident.

What is the safety benefit of this coverage?

The safety benefit is financial. It provides peace of mind that a single encounter with an irresponsible driver will not destroy your family’s financial stability or prevent you from getting the best medical care.

Is it safe to drive with only the state minimum?

No. State minimums are often outdated and insufficient for modern medical costs. UM/UIM allows you to set a safety net that reflects today’s financial reality.

Can I add this coverage to an existing policy?

Yes. You can usually add UM/UIM to your policy at any time. The cost will be pro-rated for the remainder of your policy term.