Auto Insurance News

1. Introduction

When you buy a car, your first financial priority after the purchase price is securing auto insurance. Every state has a legal threshold that you must meet to stay on the right side of the law. This is often referred to as “basic” or “minimum” insurance. People usually need this service when they are on a tight budget or when they are driving a vehicle that has a low market value.

Meeting these requirements is the bare necessity for avoiding fines, license suspension, or even vehicle impoundment. However, because these policies are stripped down, it is essential to understand exactly what you are paying for. You can use autoinsuranceplans.com to compare quotes from insurance companies to see how different levels of basic coverage fit into your monthly budget.

2. What This Service Includes

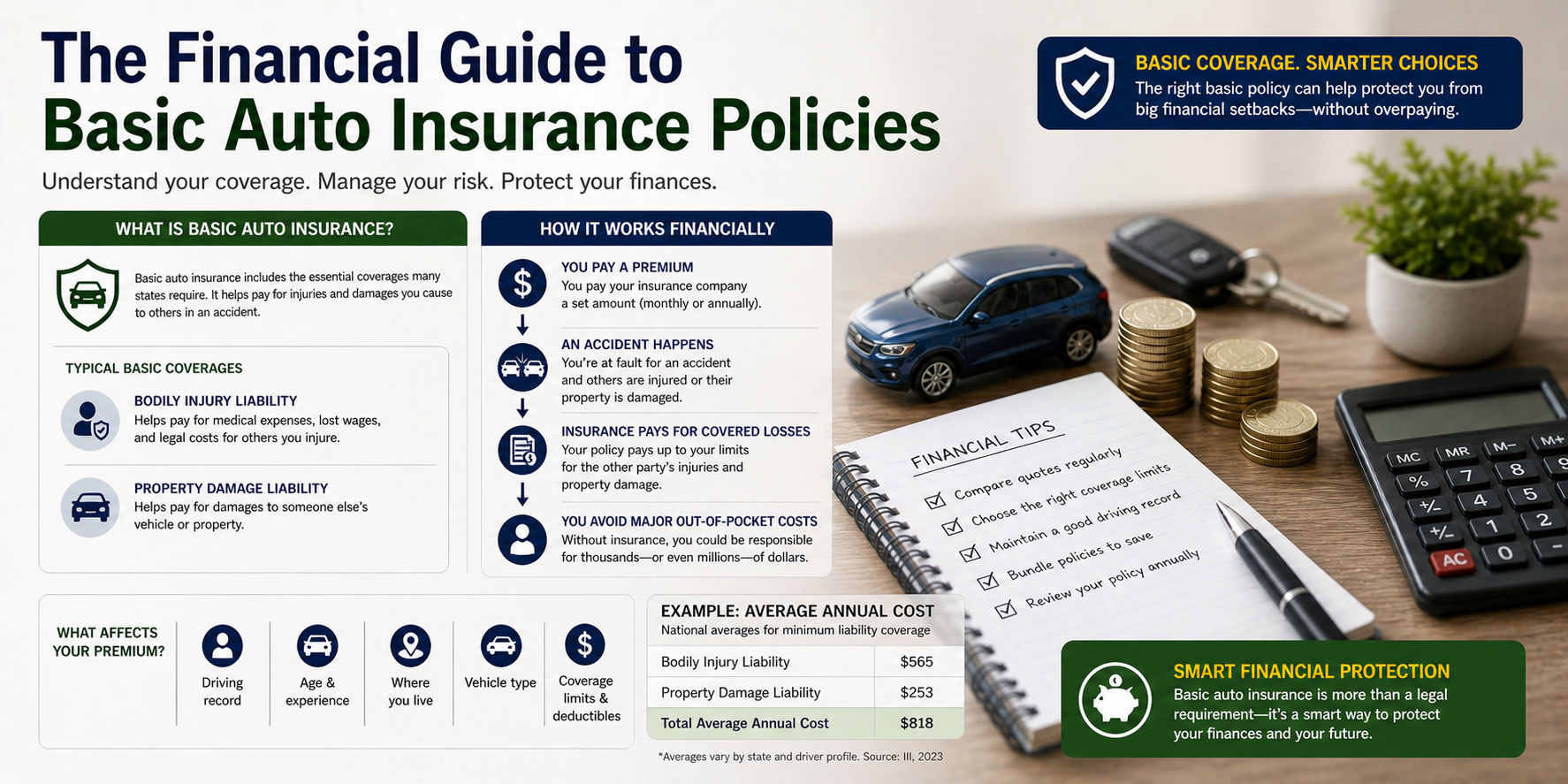

A basic auto insurance policy is essentially a liability shield. It is designed to pay for the “other guy’s” losses so that the state doesn’t have to deal with uninsured victims of car accidents.

What is typically included

A basic policy focuses on Liability. Bodily Injury Liability pays for the medical bills of others. Property Damage Liability pays for their car repairs. Some states also require a small amount of Personal Injury Protection (PIP), which covers your own medical expenses up to a very low limit. In states with high “hit and run” statistics, Uninsured Motorist coverage is often a mandatory part of this basic package to ensure you aren’t left with nothing if an illegal driver hits you.

What is usually extra or not included

The most significant exclusion in a basic policy is your own vehicle’s protection. Collision coverage, which pays for your car if you hit something, is not included. Comprehensive coverage, which pays for theft, fire, or vandalism, is also absent. If you want your insurance company to help you if your car is damaged by anything other than another insured driver hitting you, you will need to pay for these as add ons.

3. Average Cost Overview

Basic insurance is the most affordable way to drive legally. Because the insurance company has a “cap” on how much they will ever have to pay out, they can offer lower premiums.

Typical price ranges

- Typical low price range: $40 to $65 per month.

- Typical average price range: $65 to $100 per month.

- Typical high price range: $100 to $160 per month.

Simple cost summary table

| Policy Type | Monthly Price Range | Annual Price Range |

| Minimalist (Legal Only) | $40 – $80 | $480 – $960 |

| Standard Basic (Increased Limits) | $80 – $120 | $960 – $1,440 |

| Full Protection (Optional Add-ons) | $150 – $250 | $1,800 – $3,000 |

The low end of the cost spectrum is reserved for older, experienced drivers with perfect records living in low crime areas. The high end is usually for younger drivers or those living in states with “no fault” laws where the required coverage types are more numerous and expensive.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

Price is not arbitrary. Several key factors push your basic insurance costs up or down.

- Amount of coverage: Opting for the absolute lowest numbers allowed by law (like 15/30/5) will be the cheapest, but the price increases slightly if you move to 50/100/50.

- Deductible: While liability usually has no deductible, any basic policy that includes PIP or medical payments will be cheaper if you agree to a $500 or $1,000 deductible for your own medical claims.

- No fault laws: If you live in a state like New Jersey or New York, your basic policy must include Personal Injury Protection, which naturally makes the “minimum” cost higher than in a “tort” state.

- At fault history: If you have a recent accident on your record, insurers will charge you significantly more for even the most basic policy because you are a proven risk.

- Recent local references: Insurance rates can change based on recent local legislation or high rates of local accidents. Checking local quotes is the only way to get a real time price.

9. Ways to Save Money Without Cutting Corners

Saving money on insurance does not mean you have to break the law. It means being a smarter consumer.

Coverage required versus optional

The first step is to audit your policy. If you are paying for “Towing and Labor” or “Rental Reimbursement” on a basic policy, you are spending money on optional items. By cutting these, you can bring the policy down to the legal minimum and save 10% to 15%.

Comparing multiple quotes

Prices for a basic policy can vary by hundreds of dollars between companies for the exact same coverage. Some companies specialize in “high risk” basic policies, while others prefer “preferred” drivers who just want a low limit policy. Using a comparison tool is the only way to find which category you fit into.

11. Common Mistakes and Red Flags

A common mistake is selecting “minimum property damage” when you live in an area with expensive cars. If you hit a $80,000 electric vehicle and your basic policy only covers $5,000, you are in serious financial trouble.

Another red flag is “ghosting” your insurance company. If you move and don’t tell them, your policy might be invalid. Also, avoid “policy splitting” where you don’t list all the drivers in your household. If an unlisted family member crashes the car, the insurance company can legally refuse to pay the claim.

12. Frequently Asked Questions (FAQ)

Does basic insurance cover me if someone steals my car?

No. Theft is covered under Comprehensive insurance, which is almost never part of a basic or minimum state required policy.

How quickly can I get an insurance card?

Most insurers allow you to download a digital insurance card immediately after your first payment is processed online.

Will my basic insurance pay for the other person’s car?

Yes. That is exactly what Property Damage Liability is for. However, it will only pay up to the limit you selected.

Is basic insurance enough to satisfy a car loan?

Almost certainly not. Most banks and lenders require you to have Collision and Comprehensive coverage to protect their collateral.

Does a basic policy cover medical bills for my passengers?

In many states, yes, through Bodily Injury Liability or Medical Payments, but the limits are often very low on a basic policy.

What is the “at fault” impact on basic insurance?

If you are found at fault in an accident, your premium for a basic policy will likely increase by 20% to 50% at your next renewal.