Auto Insurance News

1. Introduction

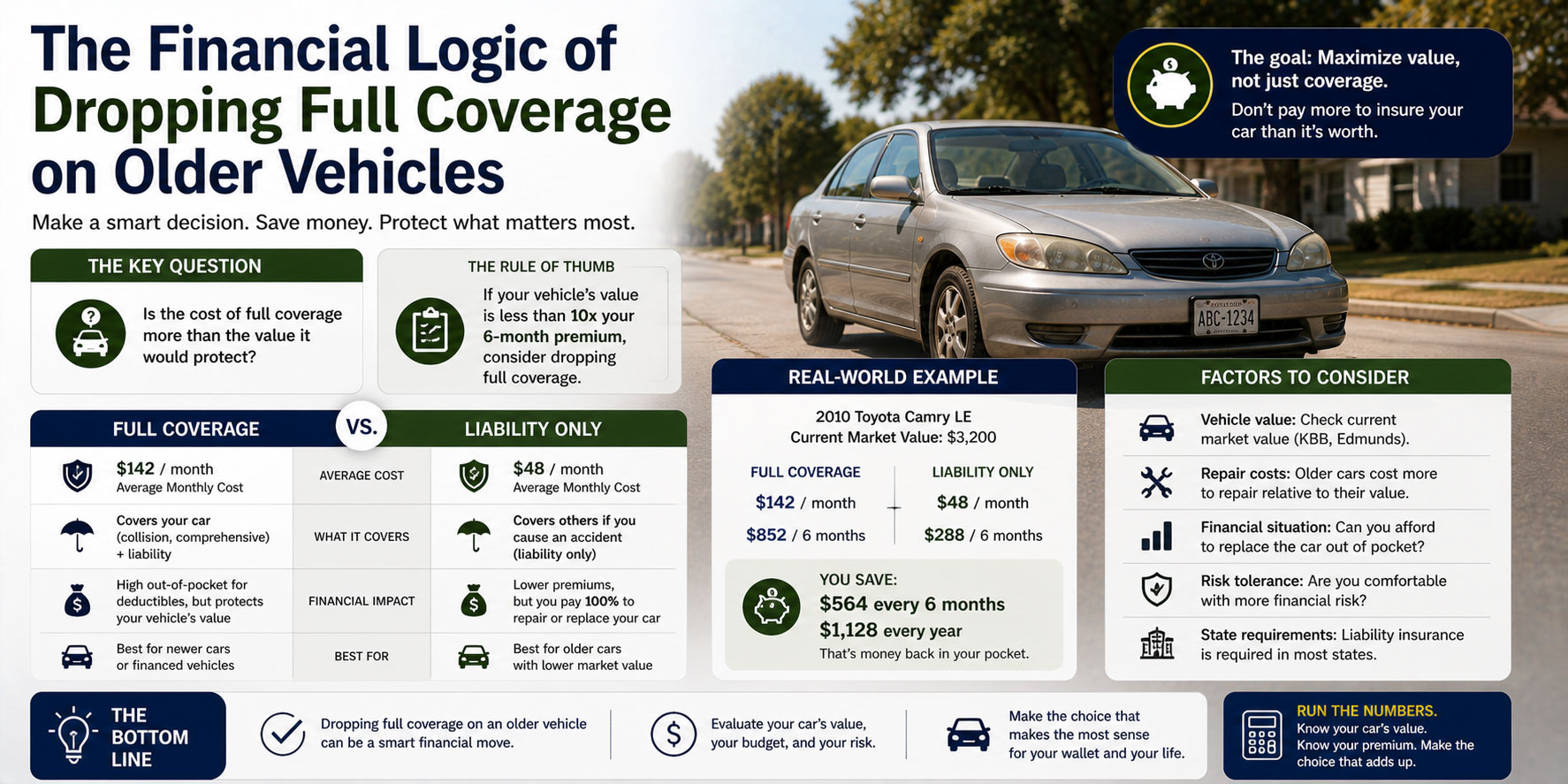

Deciding when to drop full coverage is a major financial milestone for any vehicle owner. Full coverage typically refers to the combination of collision and comprehensive insurance. While these coverages are essential for new or financed cars, their value decreases as your vehicle ages and loses market value. Most drivers begin to consider this change when the cost of the annual premium starts to approach the total value of the car itself. Making the switch at the right time can save you hundreds of dollars every year.

Before you make any changes to your policy, it is vital to see what other companies are offering. Readers can use autoinsuranceplans.com to compare quotes from insurance companies. This helps you determine if the high price of your current full coverage is an industry standard or if you could get the same protection for less elsewhere.

2. What This Service Includes

In the insurance world, full coverage is not a single service but a bundle of two optional protections added to your state-required liability insurance.

Collision Insurance

Collision coverage pays to repair or replace your vehicle if it is damaged in an accident with another vehicle or an object like a fence or a tree. It applies regardless of who was at fault. If your car is worth 5,000 dollars and you have a 500 dollar deductible, the maximum the insurer will pay for a total loss is 4,500 dollars.

Comprehensive Insurance

Comprehensive coverage handles “non-collision” events. This includes theft, vandalism, fire, or damage from natural disasters like hail or floods. It also typically covers animal strikes, such as hitting a deer. Like collision, it has a deductible and a payout limit based on the actual cash value of the car.

What Is Not Included

Dropping full coverage does not mean dropping insurance entirely. You are still required by law to carry liability insurance, which covers injuries or property damage you cause to others. Additionally, dropping full coverage means you will not have a “gap” insurance benefit, and you will not be reimbursed for your own car repairs if you are at fault in an accident.

3. Average Cost Overview

The cost of full coverage varies significantly based on your driving record and the type of car you own. On average, collision and comprehensive coverage make up about 40 to 50 percent of a total premium.

Typical Price Range for Full Coverage Add-ons

| Coverage Level | Typical Annual Price Range |

| Basic (High Deductible) | $300 to $600 |

| Standard ($500 Deductible) | $600 to $1,200 |

| Premium (Low Deductible/New Car) | $1,200 to $2,500 |

The low end of the range is usually for drivers with older cars and high deductibles. The high end is driven by expensive luxury vehicles, young drivers, or living in areas with high rates of theft and accidents. If you find your costs are in the premium range for an older car, the math rarely favors keeping the coverage.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

Several variables determine if the price you are paying for full coverage is worth the potential payout.

- The Deductible: If you have a 1,000 dollar deductible on a car worth 2,500 dollars, the insurance company is only on the hook for 1,500 dollars. This low potential payout often makes the premium cost unjustifiable.

- Amount of Coverage: Higher limits for liability do not affect the decision to drop collision, but they do increase the overall policy price.

- Window Replacement: Comprehensive insurance often covers glass. If you live in an area where cracked windshields are common, you might keep comprehensive even if you drop collision.

- At Fault vs. No Fault: In no-fault states, your own insurance pays for your medical bills regardless of the accident cause, but this is separate from the physical damage coverage of your car.

- Actual Cash Value: Insurance pays out what the car is worth today, not what you paid for it. As this value drops, the “service” you are buying becomes less valuable.

5. Ways to Save Money Without Cutting Corners

If you are not ready to drop full coverage entirely, there are ways to lower the bill without losing protection.

Raise Your Deductible

Instead of dropping collision, you can move your deductible from 250 dollars to 1,000 dollars. This can lower your premium by 15 to 30 percent. You stay protected against total losses while taking on the risk for small fender benders.

Compare Multiple Quotes

Insurance companies use different formulas to value old cars. One company might charge a high premium for an old truck, while another might offer a much lower rate. Comparing multiple quotes ensures you are not overpaying for the level of risk the car represents.

6. Common Mistakes and Red Flags

A major mistake is dropping full coverage while you still have a car loan. Most lenders require you to keep collision and comprehensive until the loan is paid in full. If you cancel it, the bank may purchase “forced placement” insurance for you, which is much more expensive and offers less protection.

Another red flag is dropping coverage when you do not have an emergency fund. If your car is totaled and you cannot afford to buy a replacement out of pocket, you may lose your ability to get to work. Only drop coverage when you have enough cash saved to buy a comparable used car if needed.

7. Frequently Asked Questions (FAQ)

What is the 10 percent rule?

If your annual full coverage premium is more than 10 percent of your car’s total value, it is generally time to drop it.

How do I find my car’s value?

Use tools like Kelley Blue Book or NADA to find the “Actual Cash Value” of your vehicle.

Will my rates go up if I drop full coverage?

No. Your total premium will decrease because you are removing a significant portion of the policy.

What happens if I get into an accident without collision?

If you are at fault, you must pay for your own repairs. If the other person is at fault, their liability insurance should pay for your car.

Does full coverage include a rental car?

Usually, rental reimbursement is an extra add-on. If you drop full coverage, you usually lose the ability to have a rental car covered after an accident.

Is there a specific age for the car when I should drop it?

Age is less important than value. However, most cars over 10 years old are candidates for liability-only insurance.

8. Call to Action for autoinsuranceplans.com

Ready to get car insurance? Ready to switch car insurance? Use autoinsuranceplans.com to compare quotes from trusted insurance companies with confidence.