Auto Insurance News

1. Introduction

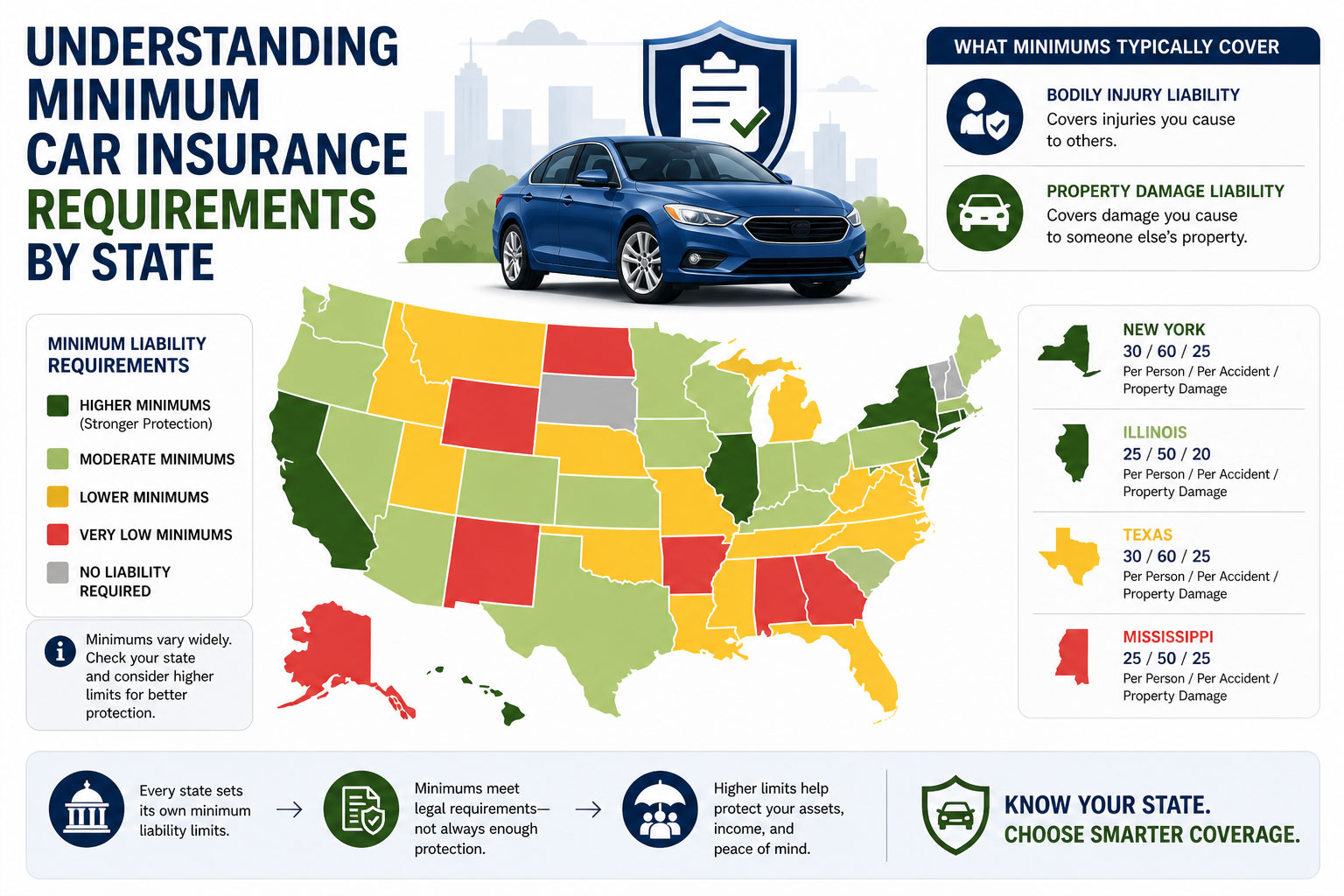

Every driver in the United States, with very few exceptions, must meet specific legal standards to operate a vehicle on public roads. These standards are known as minimum car insurance requirements. This legal baseline ensures that if you cause an accident, you have at least a basic level of financial responsibility to cover the damages or injuries sustained by others. People usually need to understand these requirements when they are buying their first car, moving to a new state, or looking to lower their monthly expenses.

While meeting the legal minimum keeps you out of trouble with the Department of Motor Vehicles, it does not always provide the protection you actually need. Navigating the specific laws of your state can be confusing because every jurisdiction sets its own limits. You can use autoinsuranceplans.com to compare quotes from insurance companies to see how these different coverage levels impact your premium. Understanding the “why” behind these laws helps you make a better decision for your wallet and your legal safety.

2. What This Service Includes

Minimum car insurance is a policy that contains only the types and amounts of coverage required by your specific state law. It is designed to protect the public from you, rather than protecting you from the world.

What is typically included

The most common component of a minimum policy is Liability Insurance. This is divided into two parts. First, Bodily Injury Liability covers the medical expenses, lost wages, and legal fees of other people if you are at fault in an accident. Second, Property Damage Liability pays for the repair or replacement of other people’s property, such as their car, a fence, or a building.

In many states, especially those with no fault insurance laws, Personal Injury Protection or Medical Payments coverage is also required. This pays for your own medical bills regardless of who caused the accident. Additionally, several states mandate Uninsured or Underinsured Motorist Coverage. This protects you if you are hit by a driver who has no insurance or whose policy limits are too low to pay for your injuries.

What is usually extra or not included

A minimum requirement policy almost never includes physical damage coverage for your own vehicle. This means Collision Insurance and Comprehensive Insurance are extra. If your car is stolen, damaged by a storm, or if you hit a tree, a minimum policy will pay zero dollars toward your repairs.

Other items that are not part of a state mandated minimum include roadside assistance, rental car reimbursement, and gap insurance. Gap insurance is particularly important if you have a loan or lease, as it covers the difference between what you owe and the car’s value if it is totaled. Most lenders will actually require you to buy more than the state minimum to protect their investment in the vehicle.

3. Average Cost Overview

The cost of a minimum insurance policy varies wildly based on where you live. Some states have very low requirements, such as $15,000 for bodily injury, while others require much higher limits. On average, a state minimum policy is significantly cheaper than a full coverage policy because the insurance company is taking on much less risk.

Typical price ranges

The following ranges represent annual premiums for drivers with a clean record and average credit.

- Typical low price range: $450 to $700 per year.

- Typical average price range: $700 to $1,100 per year.

- Typical high price range: $1,100 to $1,800 per year.

Simple cost summary table

| Coverage Level | Typical Annual Price Range |

| Basic State Minimum | $450 to $900 |

| Mid Range (Higher Limits) | $900 to $1,400 |

| Premium (Full Coverage) | $1,600 to $2,500+ |

The low end of the range is usually found in rural states with lower traffic density and lower litigation rates. The high end of the range is common in major metropolitan areas, states with high rates of uninsured drivers, or “no fault” states like Michigan or Florida where the required Personal Injury Protection can be very expensive.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

Several variables determine exactly where you fall within the price ranges mentioned above. Even for a minimum policy, insurers look at your risk profile.

- Amount of coverage: Each state has a different numeric requirement, often written as 25/50/25. If a state increases these requirements, the baseline cost for every driver goes up.

- Deductible: For liability insurance, there is typically no deductible. However, if you add optional PIP or MedPay, choosing a higher deductible can lower your premium.

- At fault versus No fault: In “tort” or at fault states, you only pay for the other person’s damage if you are wrong. In no fault states, you are required to buy expensive coverage for your own injuries, which raises the minimum cost.

- Driving record: A single speeding ticket or an at fault accident can double the cost of even a basic minimum policy.

- Location: Your zip code is a major factor. If you live in an area with high crime or frequent accidents, your “minimum” price will be higher than someone in a quiet suburb.

- Window replacement: While not usually in a minimum policy, some states like Florida or Kentucky require “full glass” coverage with no deductible, which slightly increases the base premium.

9. Ways to Save Money Without Cutting Corners

You do not have to settle for the first price you see. There are strategic ways to keep your costs down while staying legal.

Understand required versus optional

The most effective way to save is to know exactly what your state requires. If you drive an old car that is paid off, you might decide to skip Collision and Comprehensive coverage. This reduces your policy to the bare minimum required by law, which can cut your bill by 50% or more. However, you must be prepared to pay for your own repairs out of pocket.

Comparing multiple quotes

Insurance companies weigh risk differently. One company might penalize you heavily for a low credit score, while another might focus more on your years of driving experience. By comparing at least three to five quotes, you ensure you are not overpaying for the exact same legal minimum.

11. Common Mistakes and Red Flags

Many drivers make the mistake of assuming “minimum” means “full protection.” This is the most dangerous red flag. If you cause a multi car pileup and only have $10,000 in property damage coverage, you are personally responsible for the remaining tens of thousands of dollars in damage.

Another red flag is allowing your insurance to lapse. Even a one day gap in coverage can cause your future premiums to skyrocket, as insurers view uninsured periods as a major risk factor. Lastly, do not provide false information about where the car is parked. This is considered insurance fraud and can lead to a denied claim or legal trouble.

12. Frequently Asked Questions (FAQ)

What is the cheapest state for minimum car insurance?

Generally, states like New Hampshire, Maine, and Ohio tend to have some of the lowest average premiums for minimum coverage due to lower population density and fewer claims.

How long does it take to get a minimum policy?

You can usually secure a policy in under fifteen minutes online. Once you pay the first installment, coverage typically begins immediately.

Is minimum coverage safe for most drivers?

Minimum coverage is legally safe but financially risky. If you have assets like a home or savings, a minimum policy might not protect you from a lawsuit after a major accident.

What happens if I move to a state with higher requirements?

You must update your policy to match your new state’s laws within a certain timeframe, usually thirty to ninety days. Your insurance company will adjust your premium accordingly.

Does minimum insurance cover a cracked windshield?

In most cases, no. Windshield repair is usually covered under Comprehensive insurance, which is not part of the legal minimum unless your state has specific glass laws.

Can I get insurance without a driver’s license?

It is difficult but possible. You generally need to list a primary driver who has a valid license on the policy, even if you are the owner of the vehicle.