Auto Insurance News

Introduction

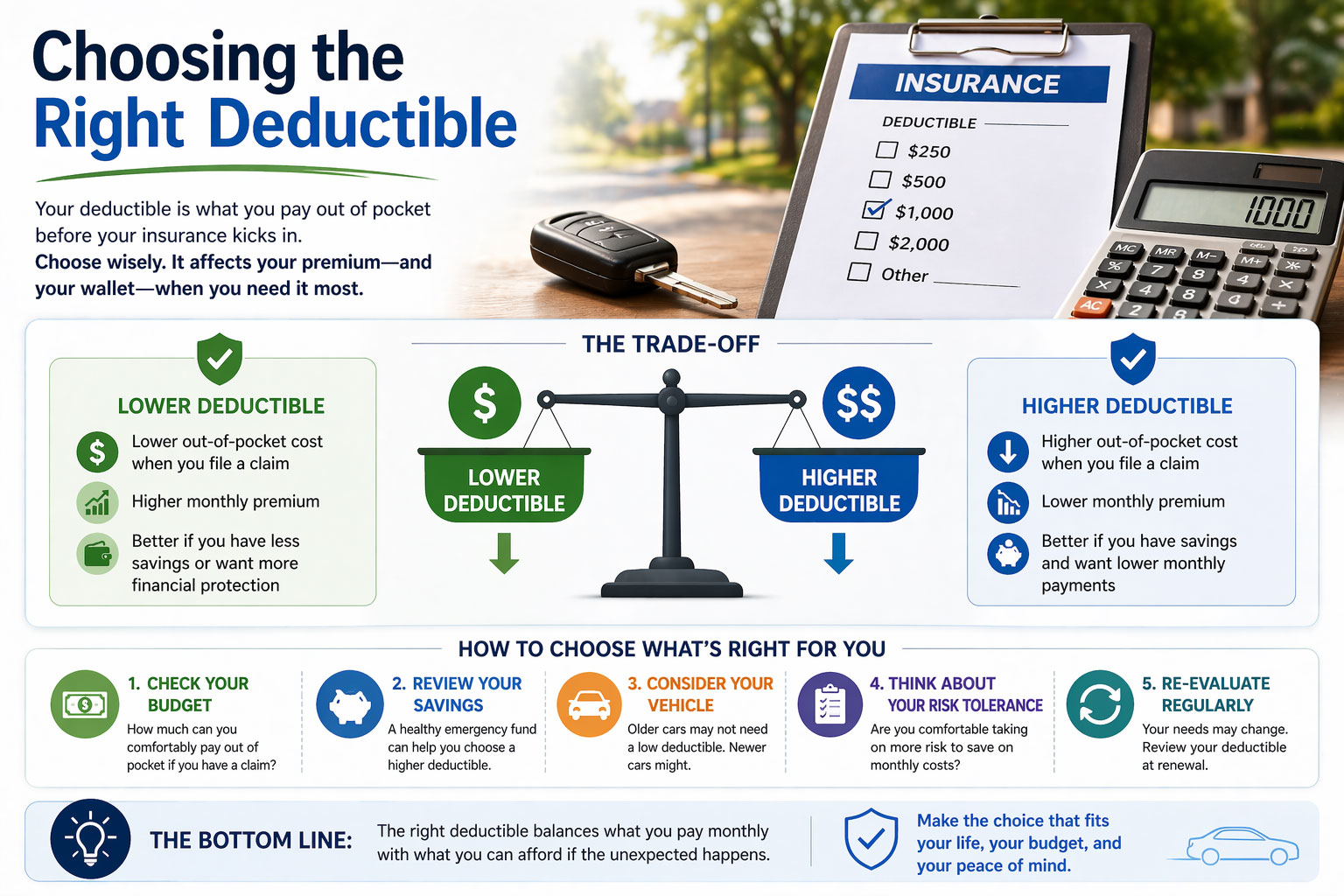

For most American drivers, the deductible is one of the least understood parts of an auto insurance policy, yet it is one of the most powerful levers you have for controlling what you pay. When you select your deductible, you are making a financial trade-off: a lower deductible means your insurer pays more after a claim, but you pay more every year in premiums. A higher deductible flips that equation.

People typically face this decision when they buy a new vehicle, finance or lease a car, shop for a new policy, or receive a renewal notice that shows a rate increase. Knowing the full picture before you decide can save you hundreds of dollars over the life of your policy.

Autoinsuranceplans.com makes it easy to compare quotes side by side from multiple insurers so you can see exactly how different deductible choices affect your final cost before signing anything.

What This Service Includes

Defining the Deductible in Plain Terms

Your deductible is a fixed dollar amount that you agree to pay when you file a covered claim. Think of it as a shared responsibility agreement between you and your insurer. The higher your agreed-upon share, the less the insurer charges you each year because their exposure on any given claim is reduced.

Deductibles apply most commonly to collision coverage and comprehensive coverage. They do not typically apply to liability coverage, which is what pays for harm you cause to other people and their property.

Typical Inclusions

Standard deductible options from most U.S. insurers range from $100 to $2,500. The most common choices are $500 and $1,000. Some carriers offer disappearing deductible programs where the amount decreases each year you go without a claim. Others offer separate deductibles for specific perils such as glass replacement, hail, or theft.

What Is Usually Separate or Not Included

Liability coverage pays third-party claims and typically has no deductible. Uninsured motorist property damage coverage may have a small deductible, often $100 to $300, depending on state law. Medical payments and personal injury protection carry their own deductible structures that vary by state. Roadside assistance and rental car coverage are add-on features that generally function without a deductible.

Average Cost Overview

The table below shows how annual premiums shift as the deductible changes for a driver with a clean record, a vehicle valued around $28,000, and coverage including both collision and comprehensive. These ranges reflect real-world averages across multiple states and carriers as of recent policy year data.

Annual Premium Estimates by Deductible Level

| Coverage / Deductible Option | Typical Annual Premium Range |

| $100 Deductible | $1,600 to $2,400 per year |

| $250 Deductible | $1,350 to $2,100 per year |

| $500 Deductible (Most Common) | $1,100 to $1,700 per year |

| $1,000 Deductible | $850 to $1,300 per year |

| $1,500 Deductible | $750 to $1,150 per year |

| $2,000 to $2,500 Deductible | $650 to $1,050 per year |

Rates on the lower end apply to drivers in suburban or rural areas, those with good credit, and vehicles with above-average safety ratings. Rates on the higher end apply to urban ZIP codes in states like California, New York, Michigan, and Florida, where traffic density, litigation rates, and repair costs drive premiums up significantly.

It is worth noting that the premium savings from a higher deductible flatten out beyond a certain point. Moving from a $500 to a $1,000 deductible typically saves more money than moving from $1,500 to $2,000.

Want to see your actual numbers? Use autoinsuranceplans.com to compare quotes with different deductible levels from top-rated insurance companies serving your ZIP code.

Key Cost Factors

Variables That Drive the Low vs. High Range

- Age and driving experience: Younger drivers, especially those under 25, pay significantly higher base rates. The deductible discount is similar in percentage terms but applied to a higher premium.

- State regulations: Michigan, Florida, and New York historically have some of the highest auto insurance rates in the country due to no-fault laws, litigation environments, and population density. Drivers in Ohio, Maine, and Idaho tend to pay much less.

- Vehicle make and model: Sports cars, luxury vehicles, and models with expensive parts cost more to insure and repair. A $500 deductible on a BMW or Tesla will yield a different premium than on a Toyota Camry.

- Annual mileage: Drivers who commute long distances or drive frequently face higher odds of a claim. Some insurers reduce premiums for low-mileage drivers, which interacts with deductible savings.

- At-fault accident history: A single at-fault accident can raise your premium by 30 to 50 percent for three to five years, depending on the insurer and state. Deductible discounts still apply but are less dramatic relative to the surcharge.

- No-fault state considerations: In states with personal injury protection mandates, your PIP pays your own medical bills regardless of fault. This adds a layer of required coverage with its own cost structure that is separate from the collision and comprehensive deductible equation.

- Credit-based insurance score: Allowed in most states, a good credit score can meaningfully lower your base premium. This amplifies the savings available through a higher deductible.

Ways to Save Money Without Cutting Corners

Required vs. Optional Coverage

Liability coverage is legally required in 49 of 50 states (New Hampshire offers an alternative proof-of-financial-responsibility option). This coverage protects others and carries no deductible in the conventional sense. What you choose on the liability limits, however, affects your overall policy cost.

Collision and comprehensive coverage are optional unless your lender requires them. Lenders and leasing companies typically mandate both and may also set a maximum allowable deductible, often $500 or $1,000. If your vehicle is paid off and worth less than $6,000, the cost-benefit analysis of maintaining full coverage may not hold up.

Smart Ways to Trim Costs

- Get at least three to five quotes before settling on a policy. Premiums for the same deductible level can vary by 40 percent or more between insurers for the same driver profile.

- Bundle your home or renters insurance with your auto policy. Most major carriers offer discounts of 5 to 25 percent for bundling.

- Ask about telematics or usage-based insurance programs. Apps that monitor safe driving habits can unlock significant discounts independent of your deductible choice.

- Increase your deductible to a level that aligns with your actual liquid savings. If you have $1,500 in a savings account earmarked for emergencies, a $1,000 deductible is realistic and safe.

- Review your coverage every year. Vehicles depreciate, and the premium savings from maintaining a low deductible on an older car diminish each year.

Common Mistakes and Red Flags

- Letting your lender set a default deductible without reviewing it: When you finance a vehicle, the dealer or lender may arrange insurance for you. The deductible they select is often not optimized for your financial situation.

- Picking a deductible based solely on monthly payment rather than total annual cost: Focus on the annual premium, not just the monthly installment. A slightly higher monthly cost for a lower deductible may or may not be worth it.

- Ignoring the break-even calculation: Divide your potential savings by the deductible increase to find how long it takes to break even. If you save $200 per year by raising your deductible by $500, you break even in 2.5 years of claim-free driving.

- Assuming all insurers price deductibles the same way: The premium benefit of a higher deductible varies widely. One carrier may save you $350 per year; another might only save $80. This is why comparison shopping is essential.

- Not accounting for glass claims: Many states have specific rules allowing zero-deductible glass claims under comprehensive coverage. Florida, for example, mandates no deductible on windshield replacement. Know your state rules.

- Overinsuring a low-value vehicle: Paying $900 per year for full coverage on a car worth $4,000 makes little mathematical sense regardless of your deductible.

Frequently Asked Questions

How much can I really save by raising my deductible?

Going from a $500 to a $1,000 deductible typically saves between $150 and $350 per year for an average driver with a midrange vehicle. Savings are higher for younger drivers and those with more expensive cars.

Is a $500 deductible the best choice for most drivers?

It is the most common choice because it balances affordable premiums with a manageable out-of-pocket cost after a claim. But it is not automatically the best choice. Drivers with solid savings may do better financially with a $1,000 or $1,500 deductible.

What is a disappearing deductible?

Some insurers offer programs where your deductible decreases by a set amount, often $100 per year, for every year you drive without a claim. This can reduce your deductible to zero over time, providing a reward for safe driving.

Does the deductible apply to each claim separately?

Yes. Each claim you file requires you to pay your deductible. If you file two collision claims in the same year, you pay the deductible twice.

Can I change my deductible after I buy the policy?

Yes. You can typically adjust your deductible at renewal or sometimes mid-policy by contacting your insurer. A change may affect your premium immediately or at the next billing cycle.

How does my deductible affect a total loss settlement?

Your deductible is subtracted from the actual cash value payment. If your car is totaled and worth $14,000 and your deductible is $1,000, you receive $13,000.

What deductible do lenders typically require?

Most auto lenders and leasing companies require a deductible no higher than $500 or $1,000 on financed or leased vehicles. Check your loan or lease agreement for the specific requirement.

Are deductibles negotiable?

You cannot negotiate a deductible below what your insurer offers, but you can choose from the options they provide. Shopping multiple insurers gives you more choices at each deductible level.