Auto Insurance News

1. Introduction

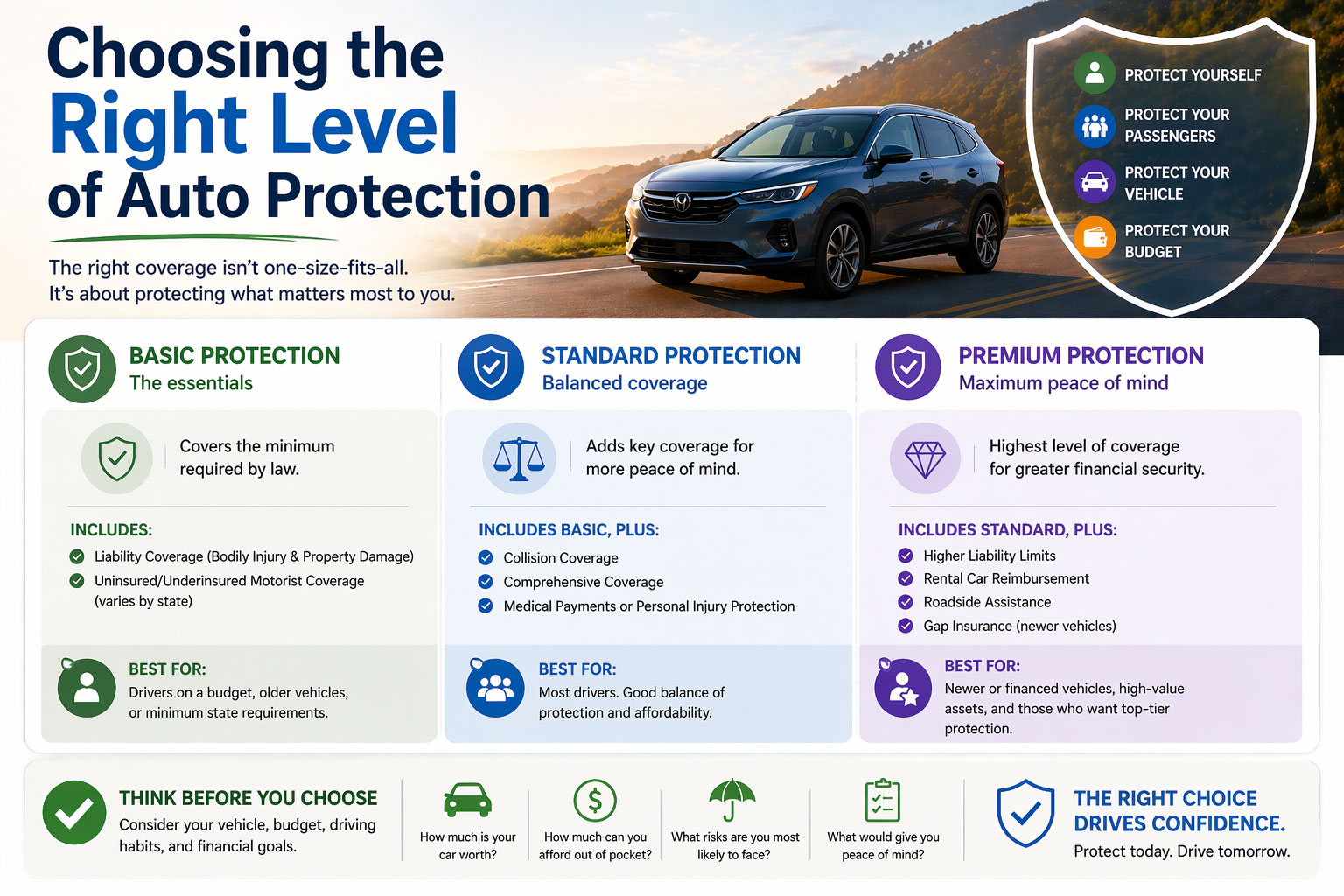

Car insurance is often viewed as a “necessary evil,” but it is actually a vital tool for protecting your financial future. Every driver must decide between a liability-only policy or a full coverage policy. Liability insurance is the bare minimum that keeps you legal. Full coverage is the safety net that ensures you can replace your car if something goes wrong.

Most drivers need to re-evaluate this choice annually. As your car ages or as your financial situation changes, the “right” amount of insurance changes with it. Using autoinsuranceplans.com allows you to see the real-time cost of these changes so you aren’t guessing about your budget.

2. What This Service Includes

When you buy an auto insurance policy, you are buying a contract. That contract specifies exactly what the insurance company will and will not pay for.

The definition of Liability

Liability insurance is the foundation of every policy. It consists of Bodily Injury (BI) and Property Damage (PD). BI pays for the other person’s hospital bills, ambulance rides, and pain and suffering. PD pays for the repairs to their vehicle. If you are in a “tort” state, the person who is at fault pays for everything. If you don’t have enough liability insurance, your personal savings and assets are at risk.

The components of Full Coverage

Full coverage is a combination of Liability plus Collision and Comprehensive.

- Collision: This covers your car if you hit another car, a guardrail, or a telephone pole. It also covers you if your car flips over.

- Comprehensive: This covers events that are usually out of your control. This includes a tree branch falling on your roof, a thief stealing your car, or a flood damaging the engine.

Exclusions and Extras

No policy covers “wear and tear.” If your transmission fails due to old age, insurance will not pay for it. Similarly, standard insurance does not cover custom equipment like expensive stereo systems or custom rims unless you add a specific “Custom Parts and Equipment” rider. Roadside assistance and rental reimbursement are also separate services that must be selected and paid for individually.

3. Average Cost Overview

Costs are driven by the total amount of money the insurance company might have to pay out. Because full coverage can result in the company buying you a whole new car, it is naturally more expensive.

Typical price ranges

- Low Range (Minimum Liability): $50 to $100 per month.

- Average Range (Standard Full Coverage): $150 to $250 per month.

- High Range (New Luxury Cars): $300 to $500+ per month.

Simple cost summary table

| Service Option | Typical Price Range (Monthly) | Best For |

| Liability Only | $50 to $90 | Older cars, low-value vehicles |

| Liability + Comprehensive | $90 to $130 | Cars in high-theft areas |

| Full Coverage | $150 to $275 | New cars, financed vehicles |

The price you see is often a reflection of your local environment. In cities with high rates of uninsured drivers, insurance companies charge more for everyone to cover the cost of accidents involving people without policies.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

Pricing is a complex calculation based on risk. Here are the variables that matter most for liability and full coverage decisions.

- Deductible: For collision and comprehensive, you must choose a deductible. Selecting a 500 dollar deductible instead of a 100 dollar one can save you 15 percent on your premium.

- Coverage Limits: Liability is often sold in sets like 25/50/25. Increasing these to 100/300/100 provides much more protection for a surprisingly small increase in price.

- Window Replacement: In states like Arizona or Florida, cracked windshields are very common. Some comprehensive policies include a “zero deductible” for glass, which increases the monthly cost slightly.

- At-Fault Status: If you have an at-fault accident on your record, insurers see you as more likely to have another one. This “risk factor” can double your liability premiums.

- No-Fault vs Tort: In no-fault states, your own insurance pays for your injuries. This adds a “Medical Payments” or “PIP” cost to every policy that drivers in other states do not have to pay.

- Credit Score: In most states, your credit history is used to determine your “insurance score.” People with higher scores are statistically less likely to file a claim and therefore get lower rates.

9. Ways to Save Money Without Cutting Corners

You can lower your insurance bill without sacrificing the coverage you actually need by being strategic.

Required versus optional coverage

The first step is to check if you are paying for things you already have. For example, if you have an AAA membership, you do not need to pay for roadside assistance through your insurance company. If you have a second car you can drive, you do not need rental car reimbursement. Removing these small items can save 10 to 20 dollars a month.

Comparing multiple quotes

Prices for the exact same level of full coverage can vary by 500 dollars or more between different companies. This is because every company has a different “appetite” for certain types of drivers. Some companies want families with minivans, while others want single professionals. Comparing quotes at autoinsuranceplans.com is the only way to find which company wants your business.

11. Common Mistakes and Red Flags

A common mistake is assuming that “Full Coverage” means you are 100 percent protected from everything. If you owe 20,000 dollars on a car that is only worth 15,000 dollars, and it gets totaled, “full coverage” only pays 15,000 dollars. You are still on the hook for the remaining 5,000 dollars unless you have gap insurance.

A major red flag is an insurance company that offers a price that is significantly lower than everyone else. If the price seems too good to be true, check the “Exclusions” page. They may be excluding common types of damage or using inferior after-market parts for repairs.

12. Frequently Asked Questions (FAQ)

Which is better, liability or full coverage?

Full coverage is always “better” for protection, but liability is better for your budget if your car is very old. A good rule of thumb is the “10 percent rule.” If your annual full coverage premium is more than 10 percent of your car’s value, consider liability.

How soon is my car covered?

As soon as you sign the documents and the payment is processed, you are covered. Most companies will email you a temporary binder immediately.

Does liability cover my own medical bills?

No. In a standard liability policy, your own medical bills are not covered. You would need Personal Injury Protection or Medical Payments coverage for that.

What happens if I hit a deer?

Hitting a deer is a comprehensive claim, not a collision claim. If you have full coverage, your car will be repaired. If you have liability-only, you pay for the repairs yourself.

Is my insurance safe if I use my car for Uber?

Not unless you have a “rideshare endorsement.” Standard personal liability and full coverage policies often exclude accidents that happen while the car is being used for commercial purposes.

Does a high deductible save money?

Yes. It lowers your monthly bill. However, it is only “safe” if you have that money sitting in a savings account ready to use at any time.