Auto Insurance News

1. Introduction

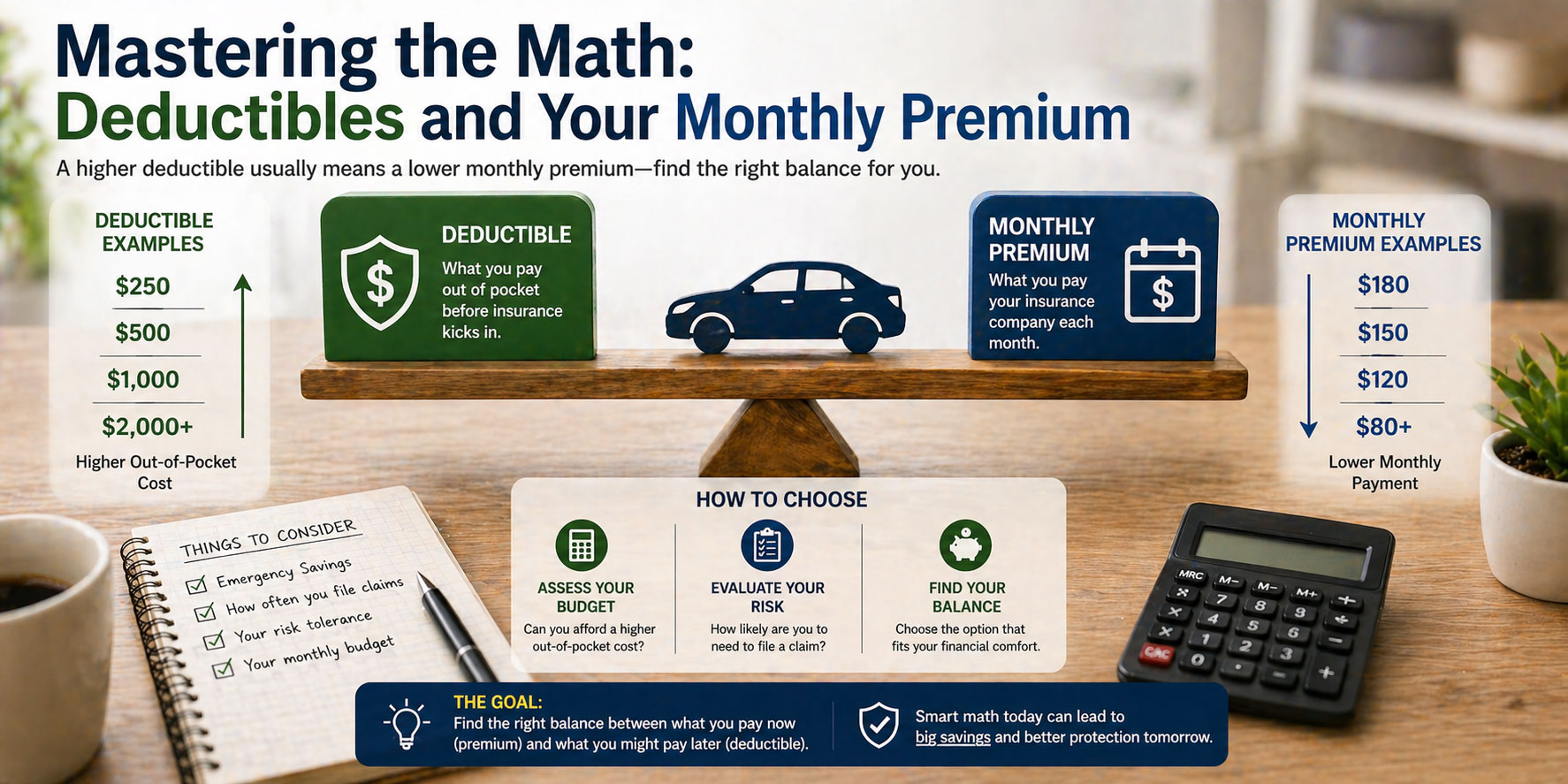

Choosing an auto insurance policy can feel like a balancing act between current costs and future risks. At the center of this balance is the deductible. This number represents your financial threshold. It is the gatekeeper that determines when your insurance company starts spending their money instead of yours. Most drivers prioritize a low monthly payment, but they often overlook how a simple change in their deductible can achieve that goal more effectively than almost any other discount.

People usually need to evaluate their deductible when they are shopping for a new policy, renewing an existing one, or experiencing a change in their financial situation. Whether you are a student on a tight budget or a professional looking to optimize your expenses, the deductible is your most powerful lever. To explore the math for your specific situation, readers can use autoinsuranceplans.com to compare quotes from insurance companies. Seeing the numbers side by side is the best way to understand the true cost of your choices.

2. What This Service Includes

When we talk about deductible selection, we are discussing the customization of your insurance contract to fit your personal risk profile.

Defining the Service in Simple Terms

The deductible is a pre-determined amount that you pay for repairs before your insurance provider covers the rest of the bill. Think of it as your “entry fee” for a claim. If you have a 500 dollar repair and a 500 dollar deductible, you pay the whole thing. If you have a 2,000 dollar repair and a 500 dollar deductible, you pay 500 and the insurance company pays 1,500.

What is Typically Included

This service is a standard part of collision and comprehensive insurance.

- Collision: Includes accidents where you hit another car, a tree, or a pole. It also covers rollovers.

- Comprehensive: Includes “acts of God” like hail or floods, along with theft, animal strikes (like hitting a deer), and vandalism.

Your choice of deductible is written into the declarations page of your policy and remains in effect until you request a change.

What is Usually Extra or Not Included

There are certain situations where a deductible does not apply or is handled differently.

- Uninsured Motorist Property Damage: Some states offer this with a low or no deductible if you are hit by someone without insurance.

- Mechanical Breakdown Insurance: This is like a warranty for your car’s engine or transmission. It often has its own separate deductible, usually around 100 dollars, which is independent of your collision deductible.

- Property in the Car: If your laptop is stolen from your car, your auto insurance might not cover it at all. These items are usually covered by homeowners or renters insurance, which has its own separate deductible structure.

3. Average Cost Overview

The financial impact of a deductible on your insurance rate is predictable but significant.

Typical Price Ranges

Insurance companies value the reduction in their risk when you take on a higher deductible.

- Typical low price range: This refers to the premium cost. High deductibles (1,000+ dollars) lead to low premiums.

- Typical average price range: The 500 dollar deductible provides a middle ground.

- Typical high price range: Low deductibles (0 to 250 dollars) lead to high premiums.

Estimated Premium Differences by Deductible

| Deductible Level | Risk to Driver | Impact on Monthly Premium |

| $0 Deductible | Very Low Risk | +25% to +40% higher than average |

| $250 Deductible | Low Risk | +15% to +20% higher than average |

| $500 Deductible | Moderate Risk | Baseline Average Rate |

| $1,000 Deductible | Higher Risk | 15% to 25% lower than average |

What Drives the Low Versus High Ends

The frequency of “nuisance claims” is the main driver. Most car repairs for minor dents and scratches cost under 1,000 dollars. If most people choose a 1,000 dollar deductible, the insurance company saves billions of dollars in small payouts and the labor costs of adjusting those claims. They pass those savings on to you in the form of lower premiums. On the high end, if you choose a 100 dollar deductible, the insurance company knows it is highly likely they will have to pay for even the smallest fender bender, so they charge you much more upfront to cover that high probability.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

When deciding on a deductible, consider these main variables that will influence your final insurance rate.

- Your Credit Score: In many states, insurance companies use credit based insurance scores. If you have a lower score, your base rate is higher, making the savings from a high deductible even more important for your budget.

- Vehicle Repair Costs: If you drive a vehicle with expensive parts, such as a Tesla or a high end German sedan, your comprehensive and collision premiums will be higher. A high deductible can help offset these costs.

- Annual Mileage: The more you drive, the higher your risk of an accident. Insurers might charge more for low deductibles if you are a high mileage driver.

- Local Reference Data: Insurance rates are highly localized. If you live in a city with a high rate of vehicle theft, your comprehensive premium will be high. Choosing a higher deductible for comprehensive coverage specifically can save you a lot of money in these areas.

- Claims History: If you have made several claims in the past three years, insurers view you as high risk. Raising your deductible is one of the few ways to keep your insurance affordable after a few mishaps.

- Driver Age: Teen drivers have the highest insurance rates. For parents of teens, choosing a higher deductible is often the only way to make adding a young driver to the policy affordable.

5. Ways to Save Money Without Cutting Corners

Optimizing your insurance budget is about being smart with your choices.

Evaluate Your Emergency Fund

The best way to save money on insurance is to build an emergency fund. If you have 1,000 dollars sitting in a high yield savings account, you can safely raise your deductible to 1,000 dollars. You “self-insure” the first thousand, and you pocket the 200 to 400 dollars a year you save in premiums. Over five years, you will have saved enough in premiums to cover the deductible itself if you ever have an accident.

Separate Your Deductibles

You do not have to have the same deductible for collision and comprehensive. Many people choose a 1,000 dollar deductible for collision (since they can control their driving) but keep a 250 or 500 dollar deductible for comprehensive (since things like hail or theft are out of their control). This targeted approach can balance cost and peace of mind.

6. Common Mistakes and Red Flags

A major mistake is failing to shop around when you change your deductible. As mentioned, different companies reward high deductibles differently. If you just change the number with your current company without checking others, you might be leaving hundreds of dollars on the table.

Another red flag is “Deductible Financing” offered by some shady repair shops. They might claim they will “waive your deductible” by overcharging the insurance company for repairs. This is insurance fraud and can lead to your policy being canceled or even legal trouble. Always pay your deductible directly and honestly.

Finally, don’t forget about your lienholder. If you are still paying off your car loan, your bank or leasing company likely requires a maximum deductible of 500 or 1,000 dollars. If you raise it to 2,000 dollars to save money, you might be in violation of your loan agreement.

7. Frequently Asked Questions (FAQ)

Does my deductible apply if my car is stolen?

Yes, if you have comprehensive coverage, you must pay your deductible before the insurance company pays out the value of the stolen vehicle.

What is a “vanishing deductible”?

It is a policy feature where the insurer reduces your deductible by a certain amount (like 100 dollars) for every year you go without an accident.

Should I file a claim if the damage is only slightly more than my deductible?

Often, the answer is no. If you have a 500 dollar deductible and the damage is 600 dollars, paying the extra 100 dollars out of pocket is usually smarter than filing a claim, which could raise your rates for years.

Does my deductible affect my liability coverage?

No. Liability coverage, which pays for damage you cause to others, almost never has a deductible.

Is it safe to have a 1,000 dollar deductible?

It is safe as long as you have 1,000 dollars accessible in case of an emergency.

Why is my comprehensive deductible cheaper than my collision deductible?

Comprehensive claims are generally less frequent and less expensive for the insurer than collision claims, so the premium reflects that lower risk.

Will my deductible be waived if the other driver hits me?

If the other driver is 100 percent at fault and has insurance, you generally won’t have to pay a deductible at all.

How does a deductible work for a windshield?

In some states, glass is covered with no deductible. In others, you must pay your full comprehensive deductible to get a new windshield.