Auto Insurance News

1. Introduction

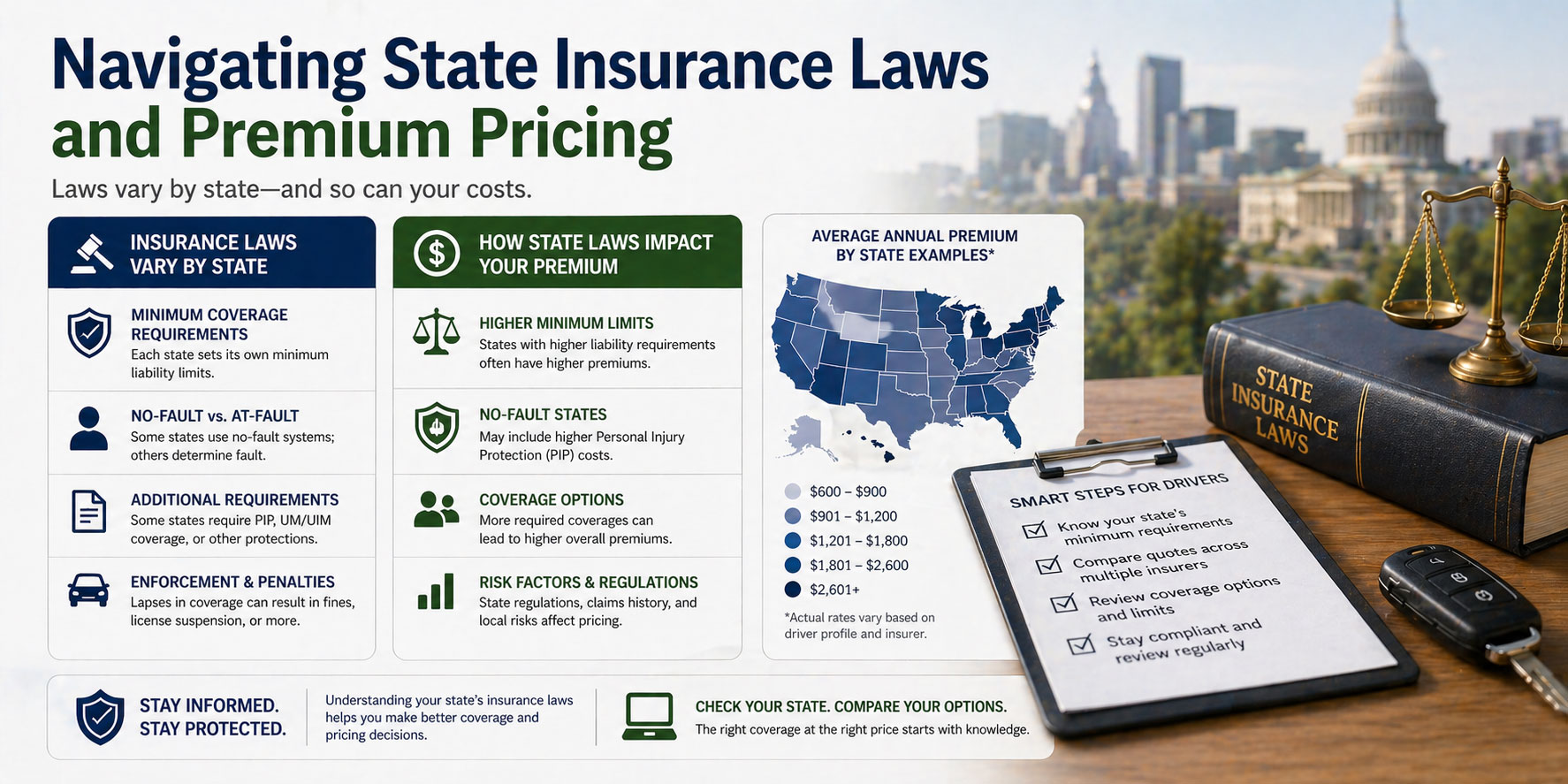

Automobile insurance is not just a personal choice, it is a legal obligation governed by state law. Every driver must adhere to their state’s minimum insurance requirements to legally use the road. People usually need to research these laws when they move across state lines or when they are trying to understand why their insurance bill changed after a birthday or a change in residence.

Because insurance is regulated at the state level, a policy in Texas looks very different from a policy in Florida or California. Navigating these complexities is easier when you have a clear roadmap of what is required and what it costs. You can use autoinsuranceplans.com to compare quotes from insurance companies to find the most competitive rates for the specific legal mandates in your area.

2. What This Service Includes

State mandated insurance is a package of specific financial protections designed to cover the costs of accidents.

What is typically included

Standard state requirements usually consist of three numbers, such as 25/50/10. The first number is Bodily Injury Liability per person ($25,000). The second is Bodily Injury Liability per accident ($50,000). The third is Property Damage Liability ($10,000). In “No Fault” states, you will also have Personal Injury Protection (PIP) included to cover your own medical costs. Some states also mandate Uninsured Motorist coverage, which pays out if you are hit by someone who is driving illegally without a policy.

What is usually extra or not included

State minimums are not designed to protect your assets or your own vehicle. Collision coverage, which handles damage to your car from an accident, is always extra. Comprehensive coverage, which handles non accident damage like fire, theft, or hail, is also extra. Furthermore, higher liability limits, which protect your personal savings from a lawsuit, are optional add ons that go beyond the basic legal requirement.

3. Average Cost Overview

The cost of staying legal depends heavily on the legislative environment of your state. Some states have “low cost” programs for low income drivers, while others have high mandatory PIP requirements that drive up the base price.

Typical price ranges

- Typical low price range: $400 to $600 per year.

- Typical average price range: $800 to $1,200 per year.

- Typical high price range: $1,400 to $2,200 per year.

Simple cost summary table

| State Category | Average Annual Premium | Average Monthly Cost |

| Low Requirement States | $450 – $750 | $37 – $62 |

| Average Requirement States | $800 – $1,300 | $66 – $108 |

| High Requirement / No-Fault States | $1,500 – $2,500 | $125 – $208 |

The primary driver of the “low” versus “high” ends of these ranges is the state’s legal system. States with “No Fault” laws are consistently the most expensive because the insurance company is required to pay for your medical bills regardless of who was wrong. States with “Tort” laws are usually cheaper because they only pay out when their driver is clearly at fault.

Ready to move forward? Use www.autoinsuranceplans.com to compare quotes from trusted local auto insurance companies so you can secure a policy with confidence.

4. Key Cost Factors

When looking at the cost of your state mandated insurance, several specific factors play a role in the final number on your bill.

- Deductible: If your state requires Personal Injury Protection or Medical Payments, you can choose a deductible. A $1,000 deductible will lower your monthly premium significantly compared to a $0 deductible.

- Amount of coverage: Each state has its own minimum. For example, California’s minimum is much lower than Maine’s. The higher the state’s legal floor, the more you will pay.

- Window replacement: In states with “Glass Buy Back” or zero deductible glass laws, the base premium for all drivers is slightly higher to account for the frequent cost of windshield repairs.

- At fault accidents: If you have been “at fault” in a recent accident, your state mandated policy will be much more expensive because you have demonstrated that you are likely to trigger the policy’s liability limits.

- No fault status: Living in a No Fault state like Michigan is one of the biggest drivers of high insurance costs in the country due to the extensive medical benefits required.

9. Ways to Save Money Without Cutting Corners

You can stay legal without going broke by using these simple strategies to manage your auto insurance expenses.

Required versus optional coverage

Be aggressive about removing what you do not need. If you have an old vehicle and excellent health insurance through your job, you should stick to the absolute minimums required by law for PIP and Medical Payments (if your state allows it). Removing Collision and Comprehensive from an old car can save you hundreds of dollars per year.

Comparing multiple quotes

Every insurance company has a different “appetite” for risk in different states. One company might be trying to grow its business in your state and offer lower rates for basic policies, while another might be raising rates to cover local losses. Comparing quotes once a year is the only way to ensure you are not paying yesterday’s high prices.

11. Common Mistakes and Red Flags

A major mistake is failing to update your insurance when you move. If you live in a different zip code than what is on your policy, the insurance company can deny your claim due to “material misrepresentation.”

Another red flag is choosing a deductible that you cannot afford to pay. If you choose a $1,000 deductible for your medical coverage to save $5 a month, but you don’t have $1,000 in the bank, you are essentially uninsured for minor injuries. Finally, never sign up with an insurance company that does not have an “A” rating for financial stability, as they may not be able to pay your claim in a major catastrophe.

12. Frequently Asked Questions (FAQ)

Does every state require car insurance?

Almost all of them do. Virginia and New Hampshire are the only two states that allow you to “opt out” under very specific, and often expensive, conditions.

What is the minimum bodily injury coverage in most states?

The most common minimum is $25,000 per person and $50,000 per accident, though some states go as low as $15,000 and others as high as $50,000 per person.

Can I buy just property damage insurance?

No. Most states require a combination of Bodily Injury and Property Damage. You cannot legally pick and choose; you must buy the whole mandated package.

How does my credit score affect my insurance cost?

In most states, insurers use a “credit based insurance score.” A lower credit score can make even a basic minimum policy cost significantly more.

Is it safe to drive with just the state minimum?

It is legal, but it is not “safe” from a financial perspective. A single serious accident can easily exceed $25,000 in medical bills, leaving you vulnerable to a lawsuit.

What is “no fault” insurance?

It is a system where your own insurance company pays for your medical bills regardless of who caused the accident, which usually leads to higher premiums for everyone.